Alright, let’s talk about gold loans. For many of us in India, they’re a quick, no-fuss way to get some much-needed cash, whether it’s for a medical emergency, a sudden business opportunity, or even just to tide over a tough month. You walk in, pledge your gold, and walk out with money. Simple, right? Well, getting the loan is just one part of the equation. The real savvy play, the one that can save you a pretty penny and a lot of stress, lies in understanding your gold loan repayment options explained properly. And trust me, there’s more to it than just paying back the principal and interest.

Here’s the thing: most people just focus on the interest rate when taking a loan. But what if I told you that how you choose to repay can be just as crucial, if not more, than the initial gold loan interest rates ? It’s true! Different repayment methods are designed for different financial situations, and picking the right one can make your journey smoother, cheaper, and less anxiety-inducing. I’ve seen countless people struggle because they didn’t know their options, or worse, chose one that didn’t fit their income flow. So, let’s dive deep, shall we? Consider this your personal guide to navigating the world of gold loan repayments.

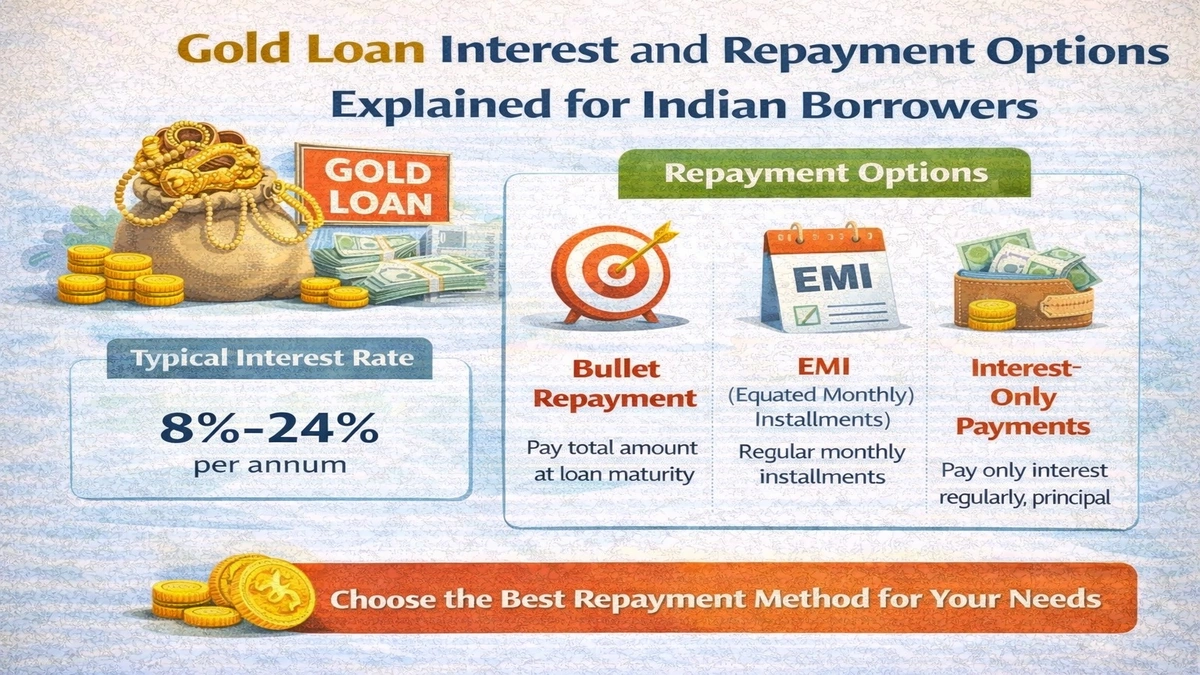

Decoding the Popular Gold Loan Repayment Schemes

When you’re looking at gold loan schemes , you’ll generally find a few standard repayment structures offered by most lenders, be it banks or NBFCs. Understanding these is your first step to making an informed decision. Don’t just nod along; ask questions, understand the nuances. Because, let’s be honest, financial jargon can be a maze, and my goal here is to cut through that for you.

First up, and perhaps the most common, is the Bullet Repayment Scheme . This one’s a bit unique to gold loans and is incredibly popular because it offers a huge relief upfront. With the bullet repayment option, you don’t pay anything – no interest, no principal – until the end of your loan tenure. You just pay everything in one go at maturity. Sounds great, right? Especially if you’re expecting a lump sum like a bonus, an inheritance, or a payment from a project. However, there’s a catch: the interest keeps accumulating throughout the period. So, while you get breathing room, the final amount can be hefty. It’s a fantastic option for short-term needs, typically up to 6-12 months, where you’re confident about a significant inflow of funds at the end. But if that lump sum doesn’t materialise, you could be in a fix.

Then we have the more traditional EMI gold loan (Equated Monthly Installment). This is what most of us are familiar with from home loans or personal loans. Here, you pay a fixed amount every month, which includes both a portion of the principal and the interest. It’s predictable, manageable, and helps you budget. This is often the preferred choice for those with a regular monthly income. It slowly reduces your principal, and you feel a sense of progress. While it might feel like a commitment, it certainly reduces the pressure of a massive payment at the end. Many prefer this for longer tenures, helping to manage their finances better and ensuring they don’t fall into a debt trap.

Another increasingly common option is the Interest-Only Payment. Here, you pay only the interest component regularly (monthly, quarterly, or even bi-annually), and the entire principal amount is paid at the end of the loan tenure. It’s a hybrid, offering the lower regular outgo of the bullet scheme but avoiding the massive interest accumulation. This can be a sweet spot for those who have some disposable income to cover interest but prefer to keep their principal untouched until a later date. It gives you flexibility without letting the interest snowball out of control.

Strategic Repayment | Making Your Gold Loan Work for You

Choosing a repayment option isn’t just about what’s available; it’s about what makes the most sense for your financial life. This is where the strategy comes in. Think of it like a game of chess; every move matters.

For instance, let’s consider the gold loan tenure . While many lenders offer flexible tenures from a few months up to 36 months, your chosen repayment method will significantly impact the total cost. A shorter tenure with a bullet repayment means less accumulated interest, but a bigger final shock. A longer tenure with EMIs spreads the burden, but you pay more interest over time. It’s a delicate balance, and honestly, the best approach is to project your income and expenses to see what feels sustainable.

What about flexibility? Many lenders offer a part payment option . This is a game-changer! If you suddenly find yourself with some extra cash – maybe a bonus, a small business profit, or even just some savings – you can use it to reduce your principal amount. Even a small part payment can significantly reduce your overall interest burden and help you repay the loan faster. This is an excellent strategy for how to repay gold loan early . Always check if your lender allows this and if there are any associated charges. Some lenders might have specific conditions or minimum amounts for part payments, so it’s wise to clarify this upfront. This kind of proactive repayment strategy, in my experience, is what separates the financially savvy from the rest.

Another crucial aspect is understanding any potential foreclosure charges . What if you want to close your loan much earlier than planned? Some lenders might levy a small fee for this, while others might not. Knowing this beforehand can influence your choice of lender and even your repayment strategy. It’s a detail often overlooked, but one that can bite you if you’re not careful.

Beyond the Basics | Tips for a Smoother Gold Loan Journey

Okay, so we’ve covered the main repayment types and some strategic considerations. But there are a few more nuggets of wisdom that can truly enhance your experience and ensure you get the maximum gold loan benefits .

Firstly, always keep an eye on your loan statement. This might sound obvious, but it’s surprising how many people don’t. Your statement will show you how much principal you’ve repaid, how much interest has accrued, and your outstanding balance. It’s your financial report card, really. Regularly checking it helps you stay on track and spot any discrepancies early.

Secondly, consider setting up automated payments. In our busy lives, missing a payment is easy. And missed payments mean penalties, increased interest, and a ding on your credit score. Setting up an auto-debit for your EMIs or interest payments ensures you never miss a due date. This isn’t just about convenience; it’s about financial discipline. This is especially useful for anEMI calculator, where consistent payments are key.

Thirdly, don’t shy away from negotiating. While gold loan interest rates might seem fixed, especially for standard products, there can sometimes be room for negotiation, particularly if you have a good relationship with your bank or if you’re a high-value customer. It never hurts to ask!

Finally, always keep an eye on the market value of gold. While this doesn’t directly impact your repayment, a significant change in gold prices could affect your ability to get a top-up loan or the loan-to-value ratio if you ever need to re-pledge. It’s about being informed, being aware, and being in control. For more insights on financial products, you might want to explore resources onsecured loans.

Frequently Asked Questions About Gold Loan Repayment

FAQs on Gold Loan Repayment

What happens if I miss a gold loan EMI or interest payment?

Missing a payment can lead to penalty charges, an increase in the effective interest rate, and potentially a negative impact on your credit score. If you anticipate difficulty, it’s always best to contact your lender beforehand to discuss possible solutions or extensions.

Can I pre-close my gold loan without penalties?

It depends on the lender and the specific loan product. Some lenders allow pre-closure without any foreclosure charges , especially after a certain lock-in period, while others might levy a small fee. Always check the terms and conditions of your loan agreement.

Is the bullet repayment scheme always the cheapest option?

Not necessarily. While it defers payments, the interest accumulates throughout the tenure. For longer tenures, an EMI or interest-only payment scheme might result in less overall interest paid, especially if you can make regular principal reductions. It’s crucial to calculate the total cost for your specific loan amount and tenure.

How can I reduce my gold loan interest burden?

The best ways are to opt for a shorter tenure, make regular part payment option s towards the principal, or choose a lender with competitive gold loan interest rates . Also, ensuring timely payments avoids penalty interest.

Are there any tax benefits on gold loan repayment?

Generally, gold loans are taken for personal or business needs and do not offer tax benefits on the principal or interest repayment like home loans or education loans. However, if the gold loan is used for business purposes, the interest paid might be deductible as a business expense. Consult a tax advisor for specific details.

So, there you have it. Choosing a gold loan isn’t just about the immediate cash; it’s about the journey of repayment. By understanding the different gold loan repayment options explained , strategizing with part payments, being aware of tenures and charges, and staying disciplined, you’re not just taking a loan; you’re making a smart financial move. Don’t let your gold loan become a burden; empower yourself with knowledge and make it work for you. Happy managing!