Ever get that nagging feeling you’re paying more than you should for your car? You know, that shiny (or not-so-shiny) vehicle sitting in your driveway, silently draining your bank account with its monthly payment? Well, my friend, you’re not alone. In the grand scheme of personal finance, understanding how to refinance car loan USA can be one of the smartest moves you make. It’s not just about lowering a number; it’s about reclaiming control of your money, your budget, and frankly, your peace of mind.

Here’s the thing: when you first bought your car, you probably got the best loan you could at the time. Maybe your credit score wasn’t stellar, or perhaps you just didn’t have the time to shop around extensively. Life happens, right? But what if I told you that your past self’s loan decision doesn’t have to dictate your financial future? That’s where car loan refinancing swoops in like a financial superhero. It’s essentially taking out a new loan to pay off your existing one, ideally with better terms. And trust me, navigating this process isn’t as scary as it sounds, especially with a clear roadmap.

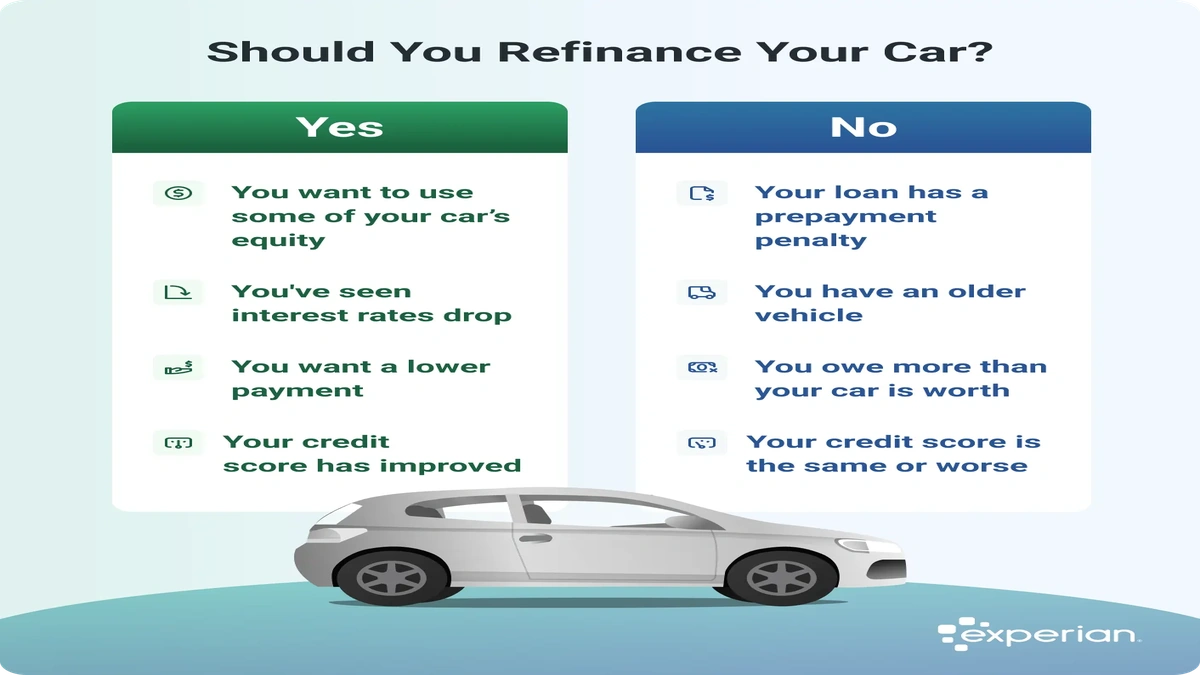

Is Refinancing Even for You? The “Why” Behind the “How”

Before we dive deep into the mechanics, let’s talk about the “why.” Why should you even considerrefinancing your auto loan? The reasons are often compelling and can lead to significant savings. One of the primary drivers is securing a lower interest rate . If your credit score has improved since you first financed your vehicle, or if market rates have dropped, you’re likely eligible for a better deal. This directly translates to lower overall costs over the life of the loan and, often, more manageable monthly payments .

But the benefits of refinancing a car loan don’t stop there. Maybe you want to reduce your monthly outlay to free up cash for other goals, like tackling student debt or boosting your savings. Refinancing can allow you to extend your loan term, reducing those payments – though a word of caution: this might mean paying more interest over the entire loan, so it’s a trade-off to consider carefully. Conversely, if you want to pay off your car faster, you could refinance to a shorter term with a slightly higher payment but save a bundle on interest. The best time to refinance car is often after a significant improvement in your credit profile or a noticeable drop in prevailing interest rates.

Your Step-by-Step Roadmap to Refinancing Success

Alright, you’re convinced. You want to explore this path to potentiallysave money. Fantastic! Now, let’s break down the refinancing process into actionable steps. Think of me as your personal guide, leading you through each turn.

Step 1 | Check Your Credit Score and Report

This is your starting line. Your credit score is the golden ticket to better car loan refinancing rates . Lenders use it to assess your risk. The higher your score, the better the rate you’re likely to receive. Pull your credit report from all three major bureaus (Experian, Equifax, TransUnion) and scrutinize it for errors. Seriously, mistakes happen, and fixing them can instantly boost your score. Knowing your score upfront also helps you set realistic expectations for the rates you might qualify for.

Step 2 | Gather Your Documents – Be Prepared!

Lenders love preparedness. Having your paperwork in order will make the process smoother than a freshly paved highway. You’ll typically need:

- Your current loan information (lender, account number, payoff amount).

- Vehicle details (make, model, VIN, mileage).

- Proof of income (pay stubs, tax returns).

- Identification (driver’s license).

- Proof of insurance.

These are the standard auto loan refinancing requirements . Having them ready means less back-and-forth later.

Step 3 | Shop Around – Don’t Settle for the First Offer!

This is perhaps the most crucial step. Don’t just go back to your original lender! Comparison shopping is your superpower here. Check with various banks, credit unions, and online lenders. Each will have different rates and terms. Use an online refinance car loan calculator to quickly estimate potential savings with different interest rates and loan terms. Remember, a difference of even half a percentage point can save you hundreds, if not thousands, over the life of the new loan .

Step 4 | Submit Your Application

Once you’ve found a few promising options, it’s time to apply. Don’t worry, submitting multiple applications for the same type of loan within a short window (usually 14-45 days) will typically only count as a single hard inquiry on your credit report, minimizing the impact on your score. Be honest and thorough with your information.

Step 5 | Seal the Deal and Enjoy the Savings

If approved, review the new loan offer meticulously. Double-check the interest rate, the loan term, any fees, and the new monthly payment. Once you’re satisfied, sign the paperwork! Your new lender will then pay off your old loan, and you’ll start making payments to them, ideally at a much better rate. Congratulations, you’ve just taken a significant step in yourfinancial journey!

Common Pitfalls and How to Dodge Them

Even with a clear guide, there are a few potholes on the refinancing road. A common mistake I see people make is extending their loan term too much just to get a lower monthly payment. While it feels good in the short term, you might end up paying more in total interest. Always consider the total cost of the loan, not just the monthly payment.

Another pitfall, especially for those navigating refinance auto loan bad credit situations, is falling for predatory lenders. If an offer seems too good to be true, it probably is. Stick to reputable financial institutions. Also, be aware of prepayment penalties on your current loan. Most auto loans don’t have them, but it’s always wise to check your original loan agreement to avoid any surprises when you pay it off early.

When Not to Refinance (Yes, There are Times!)

As much as I champion smart financial moves, there are indeed scenarios where refinancing might not be your best bet. Knowing when to refinance car loan is just as important as knowing how.

- If your current interest rate is already low: If you snagged a fantastic rate initially, you might not find anything significantly better. Don’t refinance just for the sake of it.

- If you’re nearing the end of your loan term: Most of your interest is paid at the beginning of a loan. If you only have a year or two left, the savings from a slightly lower rate might be negligible, and the hassle might not be worth it.

- If you have negative equity: This means you owe more on the car than it’s currently worth. Many lenders are hesitant to refinance a loan with significant negative equity, as it poses a higher risk for them. You might need to pay down some of the principal first.

Ultimately, the decision to refinance should always align with your broader financial goals. Is it about lowering payments, saving interest, or a bit of both? Be clear on your objective.

Conclusion | Drive Smarter, Not Harder

Refinancing your car loan isn’t about magic; it’s about smart financial strategy. It’s about recognizing that your financial situation evolves, and your loan should too. By following these steps, doing your homework, and perhaps most importantly, having the confidence to shop around, you can significantly improve your financial health. So, take the wheel, assess your options, and drive towards a future where your car payments work for you, not against you. Your wallet will thank you!

Frequently Asked Questions About Refinancing Your Car Loan

Can I refinance with bad credit?

Yes, it’s possible, but it might be more challenging. Lenders specializing in borrowers with less-than-perfect credit exist, though you might not get the absolute lowest rates. The key is to demonstrate improved financial habits since your initial loan, such as consistent on-time payments, and to shop around diligently.

How long does the refinancing process take?

Typically, the entire refinancing process can take anywhere from a few days to a couple of weeks, depending on the lender and how quickly you provide necessary documentation. Online lenders often offer a quicker turnaround than traditional banks.

Will refinancing hurt my credit score?

Initially, yes, there will be a slight, temporary dip due to a hard inquiry when lenders check your credit. However, if you secure a better loan with lower monthly payments and continue to make payments on time, your credit score is likely to improve over the long term.

What documents do I need to refinance my car loan?

You’ll generally need proof of income, your driver’s license, your current loan details (account number, payoff amount), vehicle information (VIN, mileage, make, model), and proof of insurance. Having these ready speeds up the auto loan refinancing requirements process.

How many times can I refinance my car?

There’s no strict limit to how many times you can refinance a car loan. However, each refinance involves a credit inquiry and processing. It’s generally most beneficial when there’s a significant change in your credit score or market interest rates that can lead to substantial savings.

Is there a perfect time to refinance my car loan?

The “perfect” time often aligns with an improvement in your credit score, a drop in overall market interest rates, or when you’ve paid down a significant portion of your principal, reducing your loan-to-value ratio. Essentially, it’s when to refinance car loan for maximum financial benefit.