Alright, let’s talk about money for college in the USA. It’s a huge topic, often shrouded in jargon that makes you want to pull your hair out. But here’s the thing: understanding the difference between federal student loans and private student loans isn’t just academic; it’s fundamental to your financial future. It’s the difference between a smooth sailing repayment journey and a potential financial nightmare. And trust me, you want the former.

I’ve seen countless students (and their parents) grapple with this decision, often making choices they later regret simply because they didn’t have all the facts laid out clearly. That’s why I’m here, not just to present a dry federal vs private student loans comparison USA , but to walk you through the “how” of making the right choice for your unique situation. Think of me as your guide through this financial labyrinth, pointing out the traps and the treasures.

So, let’s dive deep. How do you pick the right path? How do you ensure you’re not signing up for more than you can handle? It all starts with knowing the players.

The Grand Divide | Understanding the Core Differences

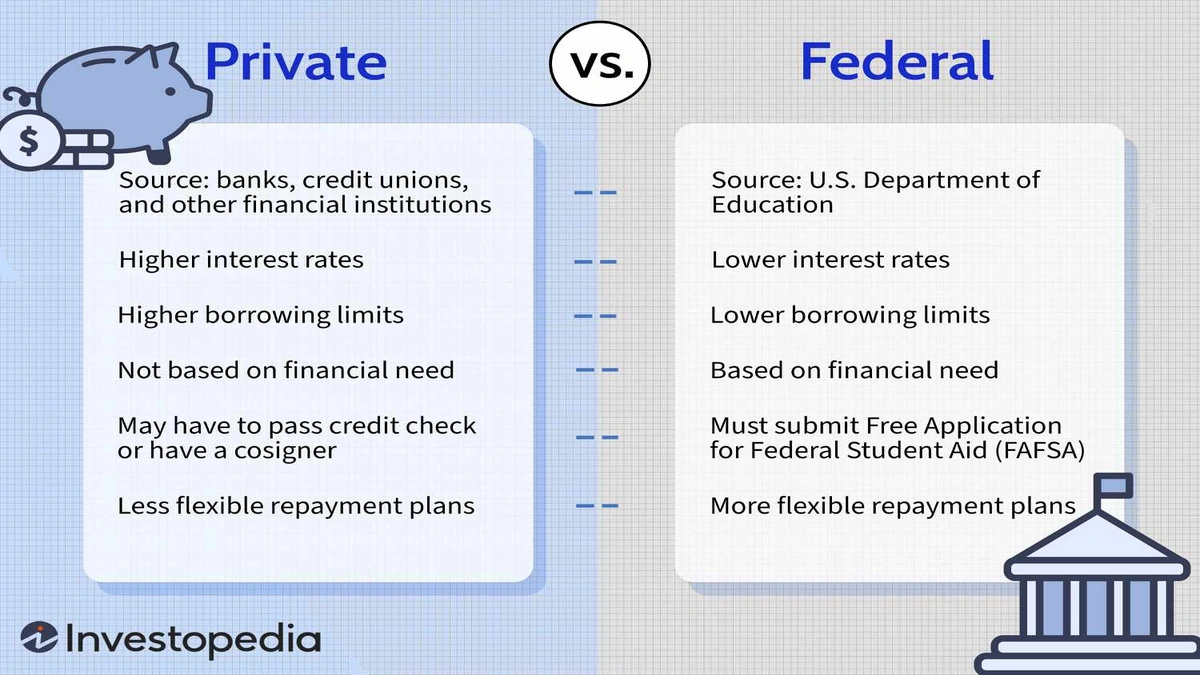

At its heart, the distinction is simple: who’s lending you the money? With federal student loans , the U.S. government is your lender. With private student loans , you’re dealing with banks, credit unions, or other private financial institutions. This single difference creates a ripple effect across everything from eligibility torepayment optionsand protections.

The first step, always, always, always , is to complete the FAFSA (Free Application for Federal Student Aid). Even if you think you won’t qualify for need-based aid, fill it out! It’s the gateway to federal loans and many scholarships. A common mistake I see people make is skipping the FAFSA because they assume their family income is too high. But guess what? Federal loans aren’t just for low-income families; they’re for nearly everyone, and the FAFSA is your ticket in.

What fascinates me about this process is how often people jump straight to private loans, lured by quick approvals or aggressive marketing, without truly exploring their federal options. It’s like opting for a risky shortcut when there’s a safer, well-trodden path right beside you. Let me rephrase that for clarity: the government generally offers better terms and more flexibility than private lenders. Period.

Federal Loans | Your Safety Net with a Catch

Think of federal loans as the ‘good guys’ of student financing. They come with a suite of borrower protections that private loans simply cannot match. Here’s why they usually win the first round:

- Fixed Interest Rates: This is huge. Your interest rates are set for the life of the loan. No sudden spikes, no surprises. This predictability makes budgeting much easier.

- No Credit Check (for most): For many federal loans, like Direct Subsidized and Unsubsidized Loans, your credit score isn’t a factor. This is a lifesaver for young students who haven’t had a chance to build credit yet.

- Income-Driven Repayment Plans: This is arguably their biggest selling point. If your income drops after graduation, you can apply for plans that adjust your monthly payments based on what you earn. This flexibility can literally save you from default.

- Deferment and Forbearance: Hit a rough patch? Lost your job? Federal loans offer options to temporarily pause your payments without defaulting. This peace of mind is invaluable.

- Loan Forgiveness Programs: While not for everyone, programs like Public Service Loan Forgiveness (PSLF) can wipe out your remaining federal loan balance after a certain number of qualifying payments if you work in public service. It’s a niche benefit, but a powerful one if it applies to you.

- Subsidized vs. Unsubsidized Loans: Federal loans come in two main flavors. With subsidized loans, the government pays the interest while you’re in school, during your grace period, and during deferment. That’s free money, folks! Unsubsidized loans accrue interest during these periods, but still offer all the other federal perks.

But, and there’s always a “but,” federal loans have borrowing limits. The government won’t lend you an unlimited amount, which is often why students look elsewhere. This leads us to the other side of the coin.

Private Loans | The Wild West of Lending

Now, let’s talk about private student loans . These are typically used to bridge the gap when federal aid and otherfinancial aidsources don’t cover the full cost of tuition. Here’s where things get a bit trickier:

- Credit-Based Approval: Private lenders are all about your credit score. If you’re a young student with little to no credit history, you’ll almost certainly need a cosigner – someone with good credit who agrees to be equally responsible for the loan. This puts a significant burden on your cosigner if you struggle to pay.

- Variable Interest Rates: Many private loans come with variable interest rates. This means your rate can fluctuate with the market, potentially making your monthly payments unpredictable and more expensive over time. While fixed-rate private loans exist, they often require excellent credit.

- Fewer Borrower Protections: This is perhaps the biggest drawback. Private lenders generally don’t offer income-driven repayment plans, generous deferment options, or loan forgiveness programs. Once you sign, those terms are pretty much set in stone.

- No Subsidies: You won’t find anything like a subsidized loan in the private market. Interest starts accruing immediately, even while you’re still in school.

I initially thought private loans were just a necessary evil for some, but then I realized how many people jump into them without understanding the long-term implications. It’s a riskier proposition, and it demands a much more cautious approach.

Making Your Move | How to Choose Wisely

So, how do you navigate this decision? It’s not about one being inherently “bad” and the other “good” (though federal leans heavily towards good). It’s about priority and necessity. Here’s my step-by-step guide:

- Maximize Federal Aid First: Seriously, exhaust every federal option before even glancing at a private lender. This means filling out the FAFSA every year, accepting all subsidized loans you qualify for, and then any unsubsidized loans you need.

- Understand Your “Need”: Sit down and calculate exactly how much money you actually need after scholarships, grants, and federal aid. Don’t borrow more than necessary. Every dollar borrowed is a dollar (plus interest) you have to pay back.

- Compare Private Lenders (If Necessary): If you absolutely must take out a private loan, shop around. Don’t just go with the first offer. Compare interest rates, fees, and repayment terms from multiple lenders. Look for fixed-rate options if possible, even if the initial rate is slightly higher.

- Consider the Cosigner Impact: If you need a cosigner, understand the responsibility you’re placing on them. Have a frank conversation about repayment expectations. A private loan can strain relationships if not handled carefully.

- Read the Fine Print: This isn’t just lawyer-speak; it’s vital. Understand the terms of your loan – when repayment starts, what happens if you miss a payment, and any fees involved.

Let’s be honest, this isn’t the most exciting topic, but making an informed decision here can literally save you tens of thousands of dollars and years of financial stress. It’s about empowering yourself with knowledge.

Beyond the Basics | Repayment, Refinancing, and Reality Checks

Once you’ve got your loans, the journey isn’t over. Repayment is where the rubber meets the road. Federal loans offer a plethora of repayment options , from standard 10-year plans to extended plans and the aforementioned income-driven plans. This flexibility is a huge safety net.

Private loans, however, are usually much more rigid. You’ll typically have a standard repayment schedule, and if you struggle, your options are limited. This is why minimizing private loan debt is almost always the smarter play.

What about refinancing? This is where you take out a new loan to pay off existing ones, often to get a lower interest rate or better terms. You can refinance both federal and private loans into a new private loan. However, a huge caveat: if you refinance federal loans into a private one, you lose all those precious federal protections like income-driven repayment and loan forgiveness . So, if you’re considering refinancing, especially federal loans, weigh the pros and cons very carefully. It might lower your interest rate, but it could strip away your safety net.

The impact on your credit score is also worth mentioning. Consistently making on-time payments, whether federal or private, will positively impact your credit. Conversely, missed payments or defaults will severely damage it, affecting your ability to get other loans (car, home) in the future.

FAQ | Your Burning Questions Answered

What is the main difference between federal and private student loans?

The main difference lies in the lender and the benefits. Federal loans are funded by the government and offer more borrower protections like income-driven repayment, deferment, and potential loan forgiveness. Private loans are from banks or private institutions, are credit-based, and offer fewer flexible repayment options and protections.

Do I need good credit for federal student loans?

For most federal student loans (like Direct Subsidized and Unsubsidized Loans), no, your credit score is not a factor. However, for a Direct PLUS Loan (for graduate students or parents), a credit check is performed, but the criteria are less stringent than for private loans.

Can I have both federal and private student loans?

Yes, absolutely. Many students exhaust their federal loan eligibility first and then turn to private loans to cover any remaining educational costs. It’s a common strategy, but always prioritize federal loans.

What if I can’t afford my student loan payments?

If you have federal loans, immediately contact your loan servicer to explore options like income-driven repayment plans, deferment, or forbearance. For private loans, your options are much more limited, but it’s still worth contacting your lender to see if any hardship programs are available, though they are rare.

Is it better to have a cosigner on a private loan?

If you have limited or no credit history, a cosigner with good credit will almost certainly help you get approved for a private loan and potentially secure a lower interest rate . However, it also makes the cosigner equally responsible for the debt, so it’s a significant commitment for them.

Should I consolidate or refinance my student loans?

Consolidating federal loans combines them into one new federal loan, simplifying payments and potentially offering new repayment plans. Refinancing (usually with a private lender) involves taking out a new private loan to pay off existing federal or private loans, often to get a lower interest rate. Be cautious with refinancing federal loans into private ones, as you lose federal protections.

Your journey through higher education funding doesn’t have to be a solo trek through dense fog. With a clear understanding of the landscape, you can make choices that empower your future, rather than burden it. Remember, knowledge is your most powerful tool in this entire process. Choose wisely, my friend, and set yourself up for financial success.