Alright, let’s grab a coffee and talk about something genuinely important for anyone dreaming of owning a home in the States: the never-ending debate between fixed vs adjustable mortgage rates USA . It’s not just a technicality, trust me. This choice can literally shape your financial future for decades. And here’s the thing: while everyone talks about the ‘what,’ I want to dive deep into the ‘why.’ Why does this choice matter so profoundly? What are the hidden implications that often get overlooked?

As someone who’s seen the ebbs and flows of the housing market, I’ve learned that understanding the underlying forces is far more powerful than just memorizing definitions. This isn’t just about picking a loan; it’s about aligning your mortgage with your life goals, your risk tolerance, and, frankly, your peace of mind. Let’s unpack it, shall we?

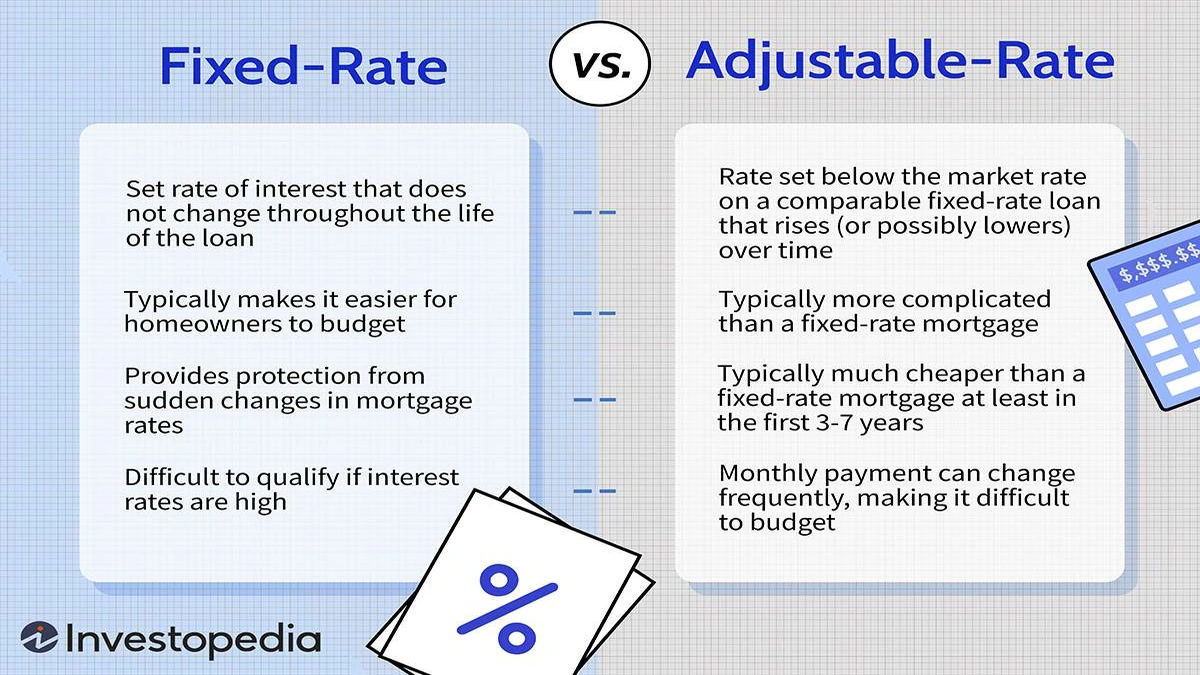

Understanding the Basics | Fixed vs. Adjustable Mortgage Rates

Before we get too deep, a quick primer. You’ve essentially got two main flavors when it comes to how your interest rate behaves over time:

- Fixed-Rate Mortgage: This is the old faithful. Your interest rate, and consequently your principal and interest mortgage payment, stays the same for the entire life of the loan – typically 15 or 30 years. It’s like setting a thermostat and forgetting about it. Predictability is its middle name.

- Adjustable-Rate Mortgage (ARM): Now, this is where things get a bit more dynamic. An ARM starts with an initial, usually lower, interest rate for a set period (say, 3, 5, 7, or 10 years). After that initial period, the rate adjusts periodically, typically once a year, based on a specific market index. Think of it as a thermostat that gets reset based on the outside temperature.

On the surface, it seems simple enough. But the ‘why’ of choosing one over the other goes far beyond these definitions.

The “Why” Behind the Rates | Decoding the Interest Rate Environment

What fascinates me is how few people truly grasp what drives these rates. It’s not just some arbitrary number plucked from the sky. The interest rate environment is a complex beast influenced by global economics, inflation, and, most critically, the Federal Reserve’s monetary policy. When the Fed raises its benchmark interest rate, it typically sends ripple effects through the entire financial system, includingcurrent mortgage rates USA. Conversely, when they lower rates, borrowing becomes cheaper.

This macro-economic dance is the invisible hand guiding your mortgage options. For a fixed-rate mortgage , you’re essentially locking in a bet on where future rates will go. If you lock in when rates are low, you’re a genius. If you lock in when rates are high and they subsequently fall, you might feel a pang of regret (thoughrefinancing optionscan often mitigate this).

For ARMs, this economic backdrop is even more critical. The initial low rate is a siren song, but the subsequent adjustments are tied directly to this fluctuating environment. If the market is experiencing significant market volatility , an ARM holder is directly exposed to that uncertainty. This is the core ‘why’ – your choice is a reflection of your outlook on economic stability and your personal comfort with risk.

Fixed Rate Mortgage Pros Cons | The Security Blanket

Let’s break down the fixed rate mortgage pros cons . For many, a fixed-rate loan is like a financial security blanket. You know exactly what your principal and interest portion of your mortgage payment will be every single month for the next 15 or 30 years. This predictability is invaluable for household budgeting and long-term financial planning .

Pros:

- Budgeting Stability: No surprises. Your major housing cost is constant. This allows for easier planning for other expenses, savings, and investments.

- Protection from Rising Rates: If interest rates soar after you’ve locked in, you’re insulated. This is a huge psychological benefit, especially in uncertain economic times.

- Simplicity: It’s straightforward. You set it and forget it. No need to constantly monitor market trends.

Cons:

- Higher Initial Rates: Fixed rates often start higher than the initial rates on ARMs, reflecting the lender’s risk of future rate increases.

- Miss Out on Falling Rates: If rates drop significantly, you’re still paying your higher locked-in rate unless you decide to refinance, which comes with its own costs.

- Less Flexibility (Initially): While you can refinance, the initial commitment is rigid.

The ‘why’ here is often about peace of mind. For many homebuyers , especially those planning to stay in their home for the long haul, the certainty of a fixed rate outweighs the potential for a slightly lower initial payment with an ARM. It’s an investment in stability.

Adjustable Rate Mortgage Pros Cons | The Calculated Gamble

Now, for the other side of the coin: the adjustable rate mortgage pros cons . An ARM can feel like a calculated gamble, offering potential rewards but also carrying inherent risks. It starts with a fixed period (e.g., 5/1 ARM means fixed for 5 years, then adjusts annually), after which the rate can fluctuate.

Pros:

- Lower Initial Payments: The most significant draw. ARMs typically offer lower interest rates during their initial fixed period compared to a 30-year fixed loan. This can make a big difference in affordability for entry-level homebuyers.

- Benefit from Falling Rates: If rates drop after your initial period, your mortgage payment could decrease, potentially saving you money.

- Good for Short-Term Ownership: If you’re confident you’ll sell or refinance before the adjustable period kicks in or significantly increases, an ARM can be a smart move.

Cons:

- Payment Uncertainty: This is the big one. After the initial fixed period, your payments can go up, sometimes significantly, leading to payment shock.

- Exposure to Rising Rates: If interest rates climb, so will your mortgage payment. This risk is amplified in a rising rate environment.

- Complex Terms: ARMs often come with caps (how much the rate can adjust per period and over the life of the loan), which can be confusing to understand.

The ‘why’ for choosing an ARM often revolves around financial strategy. Perhaps you anticipate a significant increase in income, or you’re certain you’ll move within the initial fixed period. It’s a tool for those comfortable with managing risk and closely monitoring the housing market and economic forecasts.

Who Should Choose What? Tailoring Your Financial Planning

So, how do you decide between fixed vs adjustable mortgage rates USA ? It really boils down to your personal circumstances and your outlook on the future.

- Choose Fixed If: You plan to stay in your home for many years, value predictable payments above all else, are risk-averse, or believe interest rates are likely to rise in the future. It offers unparalleled mortgage payment stability.

- Choose ARM If: You plan to sell or refinance before the initial fixed period ends, you’re comfortable with market risk, you expect your income to rise significantly, or you believe interest rates will fall (or at least remain stable) after the initial period.

I’ve seen people make both choices successfully, and I’ve seen them regret both. The key is honesty with yourself about your financial situation and future plans. Don’t just look at the initial rate; project your payments under different scenarios. Consider the stress of uncertainty versus the potential savings. This is where true financial planning comes into play.

FAQs on Fixed vs Adjustable Mortgage Rates USA

What’s the main difference in mortgage payment stability?

Q1 | What’s the main difference in mortgage payment stability?

The core difference is predictability. A fixed-rate mortgage offers consistent principal and interest payments for the entire loan term, providing complete stability. An adjustable-rate mortgage (ARM) starts with a fixed payment, but after that initial period, the payment can fluctuate based on changes in interest rates , introducing variability.

Q2 | Can I switch from an ARM to a fixed-rate mortgage?

Yes, typically you can. This is usually done through refinancing options . Many ARM holders choose to refinance into a fixed-rate loan before their adjustable period begins, especially if interest rates are favorable or if they want to lock in payment predictability. This is a common strategy to mitigate risk.

Q3 | Are ARMs always riskier?

While ARMs carry inherent interest rate risk due to their adjustable nature, they aren’t always ‘riskier’ for everyone. For someone planning to sell within the initial fixed period or with a high tolerance for market fluctuations and strong income growth, an ARM might be a suitable, even beneficial, option due to the lower initial rates. The risk depends on individual circumstances and market conditions.

Q4 | How do I know which is right for me?

Consider your long-term plans for the home, your comfort with financial risk, your current and projected income stability, and your outlook on future interest rates . If you value certainty and plan to stay put, fixed is often better. If you anticipate moving soon or your income is set to increase substantially, an ARM might be worth exploring, but always understand the caps and adjustment frequency.

Q5 | What are common ARM structures (e.g., 5/1 ARM)?

Common ARM structures include 3/1, 5/1, 7/1, and 10/1. The first number indicates the length of the initial fixed-rate period (in years). The second number indicates how frequently the rate adjusts after the initial period (e.g., ‘1’ means annually). So, a 5/1 ARM has a fixed rate for 5 years, then adjusts once a year thereafter.

The Final Word | Your Home, Your Choice

Choosing between fixed vs adjustable mortgage rates USA is one of the most significant financial decisions a homebuyer will make. It’s not about finding the ‘best’ option in a vacuum, but the ‘best’ option for you. Don’t let anyone rush you. Take the time to understand the nuances, consider your personal finances, and project how each option might play out given different economic scenarios. The ‘why’ behind your choice is deeply personal, and making an informed decision will provide a foundation of confidence for your homeownership journey, no matter what the housing market throws your way.