Picture this: You’re scrolling through car ads, your heart fluttering at the sight of that gleaming new sedan or the rugged SUV you’ve always dreamed of. The smell of fresh upholstery, the purr of the engine it’s all so close, isn’t it? But then, reality hits. The price tag. And suddenly, that dream feels a bit out of reach, clouded by questions of affordability and finances. Most of us in India don’t just walk into a showroom and pay cash, right? We look tovehicle loanoptions, and that’s where things can get, well, a little complicated.

Here’s the thing: buying a car should be exciting, not intimidating. And honestly, the single most powerful tool you have to navigate the financial maze is something often overlooked or misunderstood: the auto loan EMI calculator . It’s not just a fancy gadget; it’s your personal financial co-pilot, helping you map out your journey from dream car to driveway. Today, we’re going to peel back the layers, understand what makes this calculator tick, and discover how to use it like a seasoned financial wizard. Forget those vague estimates; we’re diving deep into the ‘how’ so you can make truly informed decisions.

What Exactly is an EMI Calculator, and Why Should You Care?

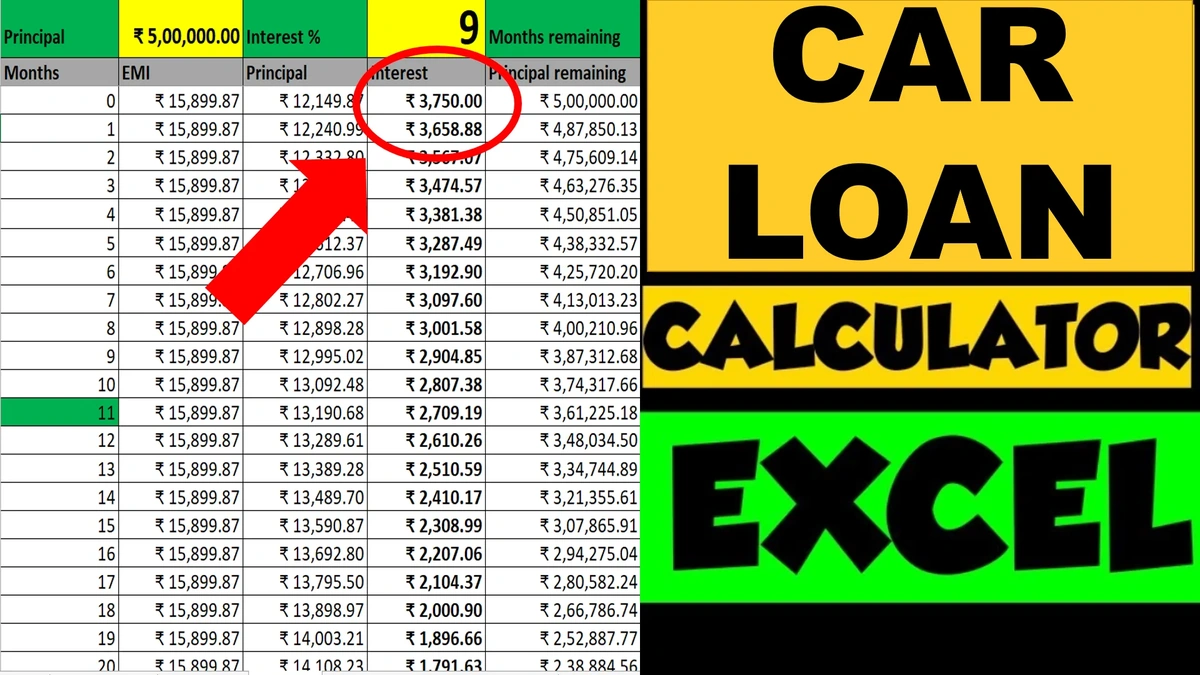

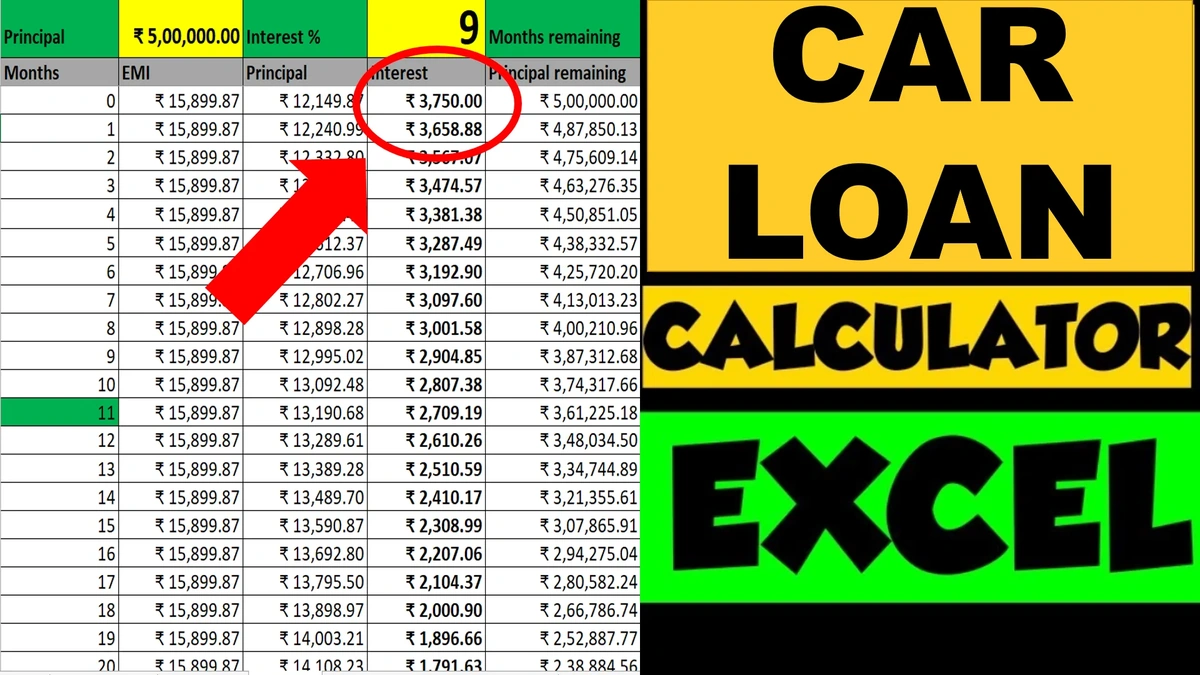

An EMI, or Equated Monthly Installment, is essentially the fixed payment you make to a lender each month until your loan is fully repaid. It covers both the principal amount (the money you borrowed) and the interest charged on it. Simple enough, right? But the magic and the confusion often lies in how that number is arrived at.

Why should you care about an auto loan EMI calculator ? Let me rephrase that for clarity: Why wouldn’t you want to know exactly how much you’ll be paying each month for the next few years? This isn’t just about budgeting; it’s about peace of mind. Without a clear picture of your monthly installment , you’re essentially driving blind into a financial commitment. A calculator allows you to input different scenarios varying loan amounts, different `car loan interest rate` figures, and crucially, different `loan tenure` options and instantly see the impact on your monthly outflow. This way, you avoid the trap of falling for a car that looks great but ties you down financially.

Think of it as test-driving the payment, not just the car. It helps you understand the commitment before you sign on the dotted line, ensuring your car dream doesn’t turn into a financial nightmare. I’ve seen too many people get carried away by the allure of a new car, only to realize later that the monthly payments are a stretch. This calculator is your reality check, but a helpful one!

Decoding the Numbers | How the EMI Calculator Works Its Magic

At its core, the auto loan EMI calculator uses a standard formula, though you don’t need to memorize it. What’s more important is understanding the inputs and their influence. Here’s a quick breakdown:

- Principal Loan Amount (P): This is the total amount of money you borrow from the bank to buy the car.

- Interest Rate (R): This is the annual `car loan interest rate` charged by the bank. For EMI calculation, it’s usually converted to a monthly rate.

- Loan Tenure (N): This is the total number of months you have to repay the loan.

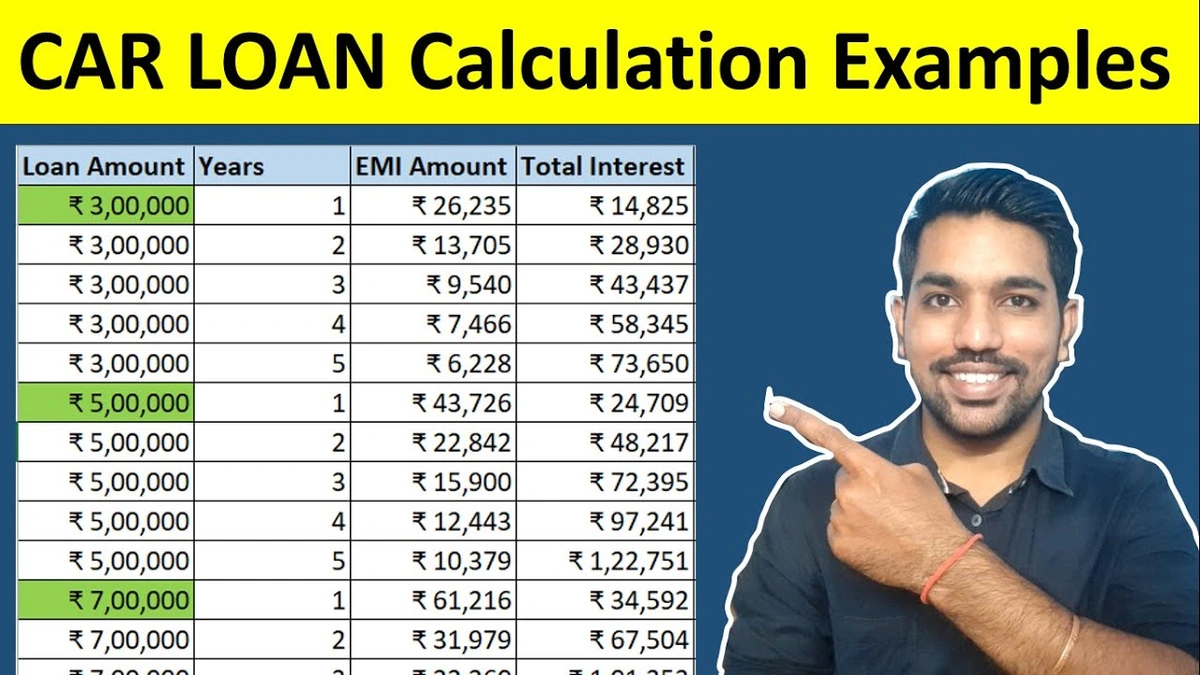

The formula essentially balances these three factors to give you a constant `monthly installment`. The longer the `loan tenure`, the lower your EMI, but and this is a big ‘but’ the more interest you’ll end up paying over the life of the loan. Conversely, a shorter tenure means higher EMIs but significant savings on interest.

Let’s be honest: many banks will try to lure you with low EMIs by stretching out the `loan tenure` for as long as possible. While a lower monthly installment might seem attractive initially, it’s crucial to use the calculator to see the total cost. This is where most people get tripped up. I initially thought a lower EMI was always better, but then I realized the true cost often hides in the extended interest payments. This insight alone can save you a pretty penny!

Another critical factor is your down payment. The larger the `down payment` you make upfront, the smaller the principal loan amount. A smaller principal directly translates to a lower EMI and, more importantly, less total interest paid. It’s like giving your future self a gift of financial freedom. Don’t underestimate its power in `car finance` planning.

Beyond the Basics | Advanced Strategies to Master Your Car Finance

Using the auto loan EMI calculator isn’t just about getting a number; it’s about strategic planning. Here are some advanced ways to leverage this tool:

Optimizing Loan Tenure for Maximum Savings

While a 7-year `loan tenure` might give you an attractive low EMI, punch in a 5-year or even a 3-year term into your calculator. You’ll instantly see the massive difference in the total interest outflow. If your budget allows, opting for a shorter tenure is almost always more financially prudent. It’s about finding that sweet spot where your monthly installment is manageable, but you’re not paying exorbitant interest for years on end. This is a classic move for smart `auto financing`.

The Power of a Higher Down Payment

We touched upon this, but let’s emphasize it. If you can push your `down payment` from 10% to 20% or even 30% of the car’s value, the impact on your car loan EMI and overall interest paid is astounding. Use the calculator to compare. See how much you save over the entire loan period. Sometimes, waiting a few extra months to save up a bigger `down payment` can translate into lakhs of rupees saved. It’s a bit of delayed gratification that pays off big time.

Exploring Pre-Payment Options

Many banks offer `pre-payment options`, allowing you to pay off a lump sum of your principal before the loan tenure ends. While some might have `pre-payment options` or foreclosure charges, using your auto loan EMI calculator in reverse can help you see the benefits. Imagine you get a bonus; instead of splurging, use the calculator to see how a partial pre-payment reduces your future EMIs or shortens your loan tenure. This proactive approach can significantly reduce your interest burden and free you from debt faster.

Understanding Your Loan Eligibility

Before you even approach a bank, using the calculator with a hypothetical car loan interest rate can help you gauge what kind of `loan eligibility` you might have. Most banks look at your income, existing liabilities, and credit score. By knowing what EMI you can comfortably afford, you can then reverse-engineer the loan amount you should be looking for. It’s about being prepared and not getting surprised by what the bank is willing to offer.

Common Pitfalls and How Your EMI Calculator Helps You Avoid Them

Even with the best intentions, car financing can be tricky. Here are a couple of common mistakes and how your trusty auto loan EMI calculator becomes your shield:

Focusing Solely on the EMI Amount

As mentioned, banks often highlight the lowest possible EMI. But a low EMI achieved through a very long `loan tenure` means you’re paying interest for a prolonged period. This significantly increases your `car finance`’s total cost. Use the calculator to compare not just the EMI, but also the total interest paid across different tenures. The stark difference might shock you, and it’s a lesson thatEquated Monthly Installmentcalculators are designed to reveal.

Ignoring Hidden Costs and Fees

Beyond the principal and interest, there are other costs: processing fees, stamp duty, insurance, registration, accessories, extended warranties, and sometimes even pre-payment charges. While the EMI calculator won’t factor in all of these directly, it helps you allocate your budget. Once you know your comfortable monthly installment , you can then factor in these additional expenses to ensure you’re not overstretching yourself. It’s about comprehensive financial planning, not just a single payment.

Impulsive Decisions Without Proper Planning

The excitement of a new car can lead to hasty decisions. An auto loan EMI calculator forces you to pause, input numbers, and see the tangible impact of your choices. It encourages thoughtful consideration over emotional buying, ensuring that the car you choose is not just a dream but also a responsible financial decision. Remember, a car is a depreciating asset, and its financing needs careful thought. It’s about making smartloanschoices in general.

Your Car Dream is Closer Than You Think | The EMI Calculator as Your Co-Pilot

Ultimately, the auto loan EMI calculator isn’t just a tool; it’s an empowerment device. It puts you in the driver’s seat of your financial journey, allowing you to manipulate variables, compare scenarios, and arrive at a `car finance` solution that truly fits your life, not just the bank’s offering. It takes the guesswork out of one of life’s significant purchases and replaces it with clarity and control.

So, the next time you dream of a new car, remember your co-pilot. Use the calculator, play with the numbers, and you’ll find that navigating the world of `auto financing` isn’t so daunting after all. In fact, it becomes an exciting part of the journey to finally parking that perfect car in your garage, knowing you made the smartest financial choice possible. Happy calculating, and even happier driving!

Frequently Asked Questions About Your Car Loan EMI

What is the ideal loan tenure for a car loan?

There’s no single “ideal” `loan tenure` as it depends on your financial situation. Generally, shorter tenures (3-5 years) mean higher EMIs but significantly less total interest paid, saving you money in the long run. Longer tenures (up to 7 years) offer lower monthly installment s but increase your overall interest cost. Use an auto loan EMI calculator to find a balance that suits your budget and saves you money.

How does a higher down payment affect my EMI?

Making a larger `down payment` directly reduces the principal amount you need to borrow. A lower principal leads to a lower car loan EMI and substantially less total interest paid over the loan period. It’s one of the most effective ways to make your `car finance` more affordable.

Can I pre-pay my car loan EMI?

Most banks allow partial or full pre-payment of your car loan EMI. However, some might levy `pre-payment options` or foreclosure charges. Always check with your lender about their specific terms and conditions before making a pre-payment to ensure it’s beneficial for you.

Does my credit score impact my car loan interest rate?

Absolutely! Your credit score is a crucial factor. A higher credit score signals lower risk to lenders, often qualifying you for a more favourable `car loan interest rate`. Conversely, a lower score might lead to higher rates or stricter `loan eligibility` criteria.

Are there any hidden charges when taking a car finance?

While the EMI covers principal and interest, other charges like loan processing fees, stamp duty, documentation charges, and sometimes even pre-payment penalties might apply. Always ask for a detailed breakdown of all associated costs before finalizing your car finance deal to avoid surprises.

How can I improve my loan eligibility?

To improve your `loan eligibility`, focus on maintaining a good credit score, reducing existing debts, ensuring a stable income, and having a lower debt-to-income ratio. A higher `down payment` also significantly boosts your chances of securing a good car loan interest rate.