Let’s face it, the dream of owning a home in the USA is a powerful one. But for many, especially first time home buyers , that initial hurdle – the down payment, the closing costs – feels less like a hurdle and more like an insurmountable mountain. You’ve probably heard whispers about ‘grants’ or ‘assistance programs,’ but navigating that maze can feel overwhelming, right? Well, take a deep breath. Because by the end of this chat, you’ll have a clear, actionable roadmap to finding and securing first time home buyer grants USA 2026 . I’m here to be your guide, cutting through the jargon and showing you exactly how to make that dream a reality. We’re going to demystify the process, explain the nuances of various programs, and equip you with the knowledge to confidently approach your home buying journey with the added benefit of significant financial assistance .

Decoding the Grant Landscape | Federal vs. State Programs

Here’s the thing about first time home buyer grants : they aren’t a single, uniform thing. Think of it like a vast ocean with many currents – some federal, some state, and even some local. Understanding these currents is your first step. On one hand, you have federal housing grants and programs, often originating from agencies like HUD (the Department of Housing and Urban Development). These typically set broad guidelines and sometimes provide funds that trickle down to states. It’s a bit like the federal government laying the groundwork, but the real action often happens closer to home.

Then there are the state-specific homebuyer programs . These are often the true goldmines for down payment assistance and closing cost help. Each state, and sometimes even counties or cities within them, will have its own unique set of programs designed to help its residents. This is where your diligent research really pays off, because what works in California might be totally different in Texas. What fascinates me is how these programs are tailored to local housing market conditions and specific community needs, creating a diverse landscape of opportunities. For example, some states might prioritize assistance in rural areas, while others focus on urban revitalization. It’s a complex ecosystem, but incredibly rewarding once you know where to look. You can find a wealth of information directly from official sources like HUD.gov , which outlines many federal initiatives and resources.

Are You Eligible? Navigating the Criteria for First-Time Home Buyer Grants

Now, let’s get real about eligibility. This isn’t a free-for-all, and honestly, that’s a good thing – it means these programs are targeted to those who truly need them. The term ” first time home buyer ” itself is often misunderstood. Generally, it means you haven’t owned a primary residence in the last three years. But even if you owned a home years ago, you might still qualify! There are nuances, such as for single parents or those who previously owned a home that wasn’t affixed to a permanent foundation. It’s always worth checking the specific program details.

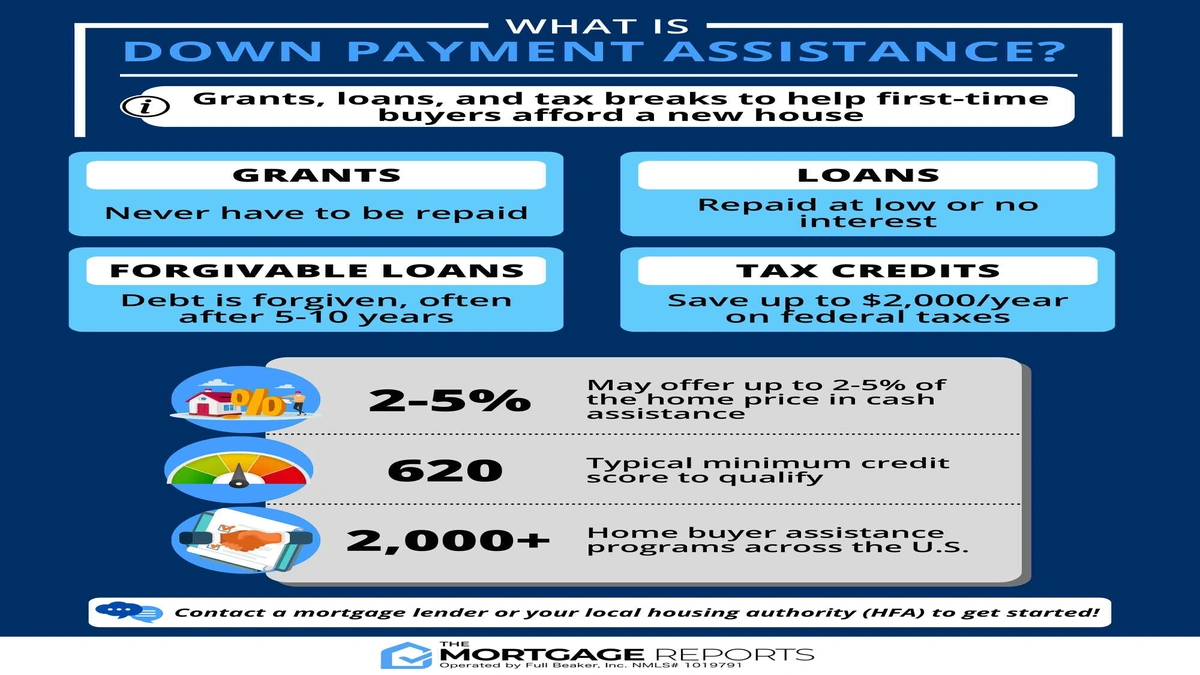

Beyond that, expect income limits. These aren’t designed for millionaires, but for moderate to low-income families. The limits vary significantly by location and family size, so don’t just guess; look up the exact figures for your area. Your credit score impact is also a big deal; while some programs are more flexible, a healthier score (typically above 620-640 for many programs) always opens more doors and can secure you better interest rates. You’ll also likely encounter purchase price limits on the homes you can buy, ensuring the grants are used for reasonably priced properties, and sometimes even requirements to complete a homebuyer education course. This course, by the way, isn’t just a hoop to jump through; it’s genuinely valuable, teaching you about budgeting, maintenance, and what to expect during your entire home buying journey . It’s all about setting you up for success, not just getting you into a house, and I’ve seen countless people benefit immensely from these insights.

Beyond the Grant | Understanding Your Mortgage Options

Here’s a crucial insight: grants rarely stand alone. They almost always work in conjunction with a mortgage. So, while you’re hunting for those first time home buyer grants USA 2026 , you also need to understand the different types of mortgage options available. You’ve probably heard of FHA loans, VA loans, and USDA loans. These are fantastic for first time home buyers because they often come with lower down payment requirements or more flexible credit criteria. FHA loans, for instance, are insured by the Federal Housing Administration and are very popular, requiring as little as 3.5% down. VA loans are a huge benefit for veterans and active-duty service members, often requiring no down payment at all. USDA loans are for designated rural areas and can also offer 100% financing.

Even conventional loans, which are not government-backed, can be paired with down payment assistance programs. The key is finding a lender who specializes in these programs. They’re like navigators who know all the hidden coves and currents in the vast sea of mortgage lending. They can help you determine the best loan product that complements the grants you qualify for, optimizing your overall financial assistance package. This integrated approach is what truly unlocks homeownership for many.

Your Step-by-Step Action Plan to Secure Grants in 2026

Okay, enough talk about what is . Let’s talk about what to do . This is your practical guide, your ‘how-to’ for making those first time home buyer grants a reality. I’ve seen these steps work wonders, so let’s walk through them together.

- Research, Research, Research: Start with your state’s housing finance agency (HFA). A quick Google search for ‘[Your State] Housing Finance Agency’ will usually lead you right there. They are the primary hub for state grants and often have comprehensive lists of programs, eligibility criteria, and participating lenders. Don’t stop there; also check city and county websites. Sometimes local programs offer even more tailored financial aid. Every little bit helps, right?

- Get Pre-Approved for a Mortgage: This isn’t just a suggestion; it’s a non-negotiable step. A pre-approval letter tells you how much you can realistically afford and shows sellers you’re serious. More importantly, it helps you understand which mortgage options you qualify for, which then dictates which grants can be layered on top. Think of it as getting your base camp set before you start climbing.

- Find a Grant-Savvy Lender: Not all lenders are created equal when it comes to grants. Seek out mortgage brokers or loan officers who explicitly advertise their expertise in first time home buyer programs and down payment assistance. They often have direct relationships with state and local housing agencies and can guide you through the specific paperwork and timelines. They are invaluable for your home buying journey.

- Complete Homebuyer Education (If Required): As mentioned, many programs require this. Embrace it! These courses are designed to empower you, giving you the knowledge to be a confident homeowner. I initially thought these were just bureaucratic hurdles, but then I realized how much practical, real-world advice they offer.

- Apply and Be Patient: Once you’ve found the right program and lender, the application process begins. It requires attention to detail, gathering financial documents, and sometimes a bit of waiting. But trust me, the payoff is absolutely worth it.

And a quick thought: if you’re exploring all your financial avenues for your home purchase, sometimes people look into things like instant personal loan online options for smaller, immediate needs, though this is separate from the grant process itself. Just keep all your options open and understand their implications for your overall financial planning for home purchase .

The Fine Print | What to Watch Out For

Now, let’s talk about the details that often trip people up. While first time home buyer grants USA 2026 are fantastic, they’re not always a simple handout. You need to understand the fine print. This is where your analytical hat comes on, because the devil is truly in the details.

- Forgivable vs. Repayable: Some grants are truly ‘free money’ – they are forgiven after a certain period (e.g., 5-10 years) as long as you remain in the home. Others are structured as ‘silent second mortgages’ or ‘deferred loans’ that you might have to repay if you sell or refinance before a specific term, or even repay in full when you sell. Always, always clarify this upfront. It’s the single most important question to ask!

- Recapture Clauses: This is less common but important to know. A recapture clause means if you sell your home for a significant profit within a certain timeframe, you might have to repay some of the grant money. It’s designed to prevent people from using grants just to flip houses and ensures the funds go to those genuinely seeking long-term homeownership.

- Property Type Restrictions: Some programs might have restrictions on the type of home (e.g., single-family, condo, multi-family) or its condition. Don’t assume every grant applies to every property type.

- Home Value Limits: We touched on this, but it’s worth reiterating. Most programs have limits on the maximum purchase price of the home, which is tied to the local housing market conditions. This ensures the grants support affordable housing goals.

Always read every document thoroughly and ask your lender for clarification on anything you don’t understand. A helpful resource for understanding various financial products and consumer rights is the Consumer Financial Protection Bureau . And hey, if you’re ever in a situation where traditional loan approvals are a challenge, perhaps because of unique income situations, it’s worth knowing that there are resources out there discussing home loan approval no income proof USA , though this is generally for different types of loans and often comes with its own set of considerations, usually not directly linked to standard grant programs. Just something to keep in mind as you explore the broader financial landscape.

Frequently Asked Questions About Home Buyer Grants

Let’s tackle some common questions I hear about first time home buyer grants .

What exactly qualifies me as a first time home buyer?

Generally, you’re considered a first time home buyer if you haven’t owned a primary residence in the last three years. However, there are exceptions, like single parents, displaced homemakers, or those who previously owned a home not affixed to a permanent foundation. Always check the specific program’s definition!

Are these grants truly “free money”?

Many are! Particularly those that are fully forgiven after a certain occupancy period. But some, as we discussed, are structured as deferred loans or silent seconds that may require repayment under specific circumstances, often if you sell the home too soon. Always clarify the terms before accepting.

How much down payment assistance can I expect?

This varies wildly. It could be a flat amount (e.g., $5,000), a percentage of the home’s purchase price (e.g., 3-5%), or even cover all your closing costs . Some programs can offer tens of thousands of dollars, especially in higher-cost areas. It truly depends on the program and your eligibility.

Can I combine multiple federal housing grants?

It’s rare to combine multiple federal grants for the same purpose, but it’s very common to combine a federal loan program (like FHA) with a state or local down payment assistance grant. Your lender will be the best resource for navigating these combinations.

Where do I start looking for state grants in my area?

Your best starting point is your state’s Housing Finance Agency (HFA). Most states have one, and their websites are usually comprehensive resources for all available state-specific homebuyer programs . You can also consult local government housing departments.

The journey to homeownership can feel daunting, but with the right information and a proactive approach, those first time home buyer grants USA 2026 are absolutely within reach. Remember, you’re not alone in this. There are programs, people, and resources designed to help you cross that threshold. So, arm yourself with knowledge, connect with the right professionals, and start building your future. Your dream home isn’t just a dream; it’s a very real possibility, and with these grants, it might be closer than you think. Happy house hunting!