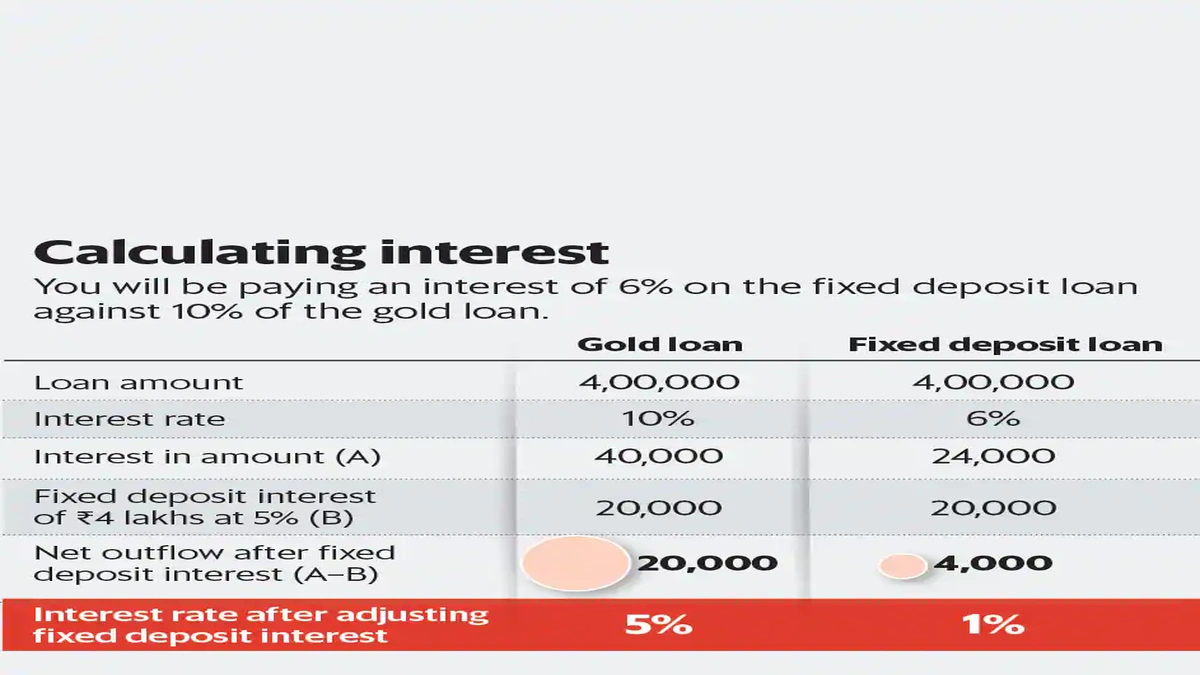

Alright, let’s be honest. When you hear “interest calculation formula,” does your brain immediately switch off? Mine used to, too! But here’s the thing about gold loans in India: they’re a lifeline for millions, offering quick access to funds by leveraging an asset most Indian households cherish – gold. Yet, a lot of us dive in without truly understanding the engine under the hood: the gold loan interest calculation formula.

It’s not just about knowing the current gold loan interest rates; it’s about understanding how those rates translate into actual money out of your pocket. Think of me as your friendly neighborhood financial guide, sitting across from you with a cup of chai, ready to demystify this crucial aspect. We’re going to break down the ‘how’ of it all, so you can make smarter decisions, save money, and never feel lost in the financial jargon again. Because, truly, knowing this formula is like having a superpower in your financial toolkit.

Ever Wondered How Your Gold Loan Interest Is Really Calculated?

Many assume it’s just a simple percentage, right? You borrow X amount, they charge Y percent, and boom, that’s your interest. Well, not quite. While the core concept is straightforward, the nuances in various gold loan schemes and repayment options can significantly alter your total outflow. The interest isn’t just a number; it’s a dynamic figure influenced by several factors affecting gold loan interest.

The primary goal here isn’t to turn you into a mathematician, but to empower you with enough knowledge to confidently use a gold loan calculator and even do a quick mental check. We’ll look at the principal amount, the tenure of the loan, the type of interest (simple vs. compound, though most gold loans favour simple interest to keep things transparent), and the all-important Loan-to-Value (LTV) ratio. Understanding these elements is the first step in mastering the gold loan interest calculation formula.

Deconstructing the Basics | What Drives Gold Loan Interest Rates?

Before we jump into the actual formula, let’s quickly dissect what makes those interest rates tick. It’s not arbitrary, I promise!

- Loan Amount & LTV: The amount you borrow, directly linked to the value of your gold, plays a huge role. Lenders typically offer a percentage of your gold’s market value (the LTV). A higher LTV might sometimes mean slightly higher interest rates due to increased risk for the lender.

- Tenure: The loan duration matters. Shorter tenures often have different rate structures than longer ones.

- Repayment Frequency: Some lenders offer monthly, quarterly, or even bullet repayment options. This choice impacts how frequently interest accrues.

- Lender Type: Banks, NBFCs (Non-Banking Financial Companies), and even unorganised lenders (which I’d generally advise against due to lack of regulation) all have different rate structures. Always compare the best gold loan rates from reputable institutions.

- Market Conditions: General economic conditions, RBI policies, and even gold price volatility can indirectly influence rates.

So, when you see a rate advertised, remember it’s a product of these interwoven factors. It’s never just a standalone number.

The Nitty-Gritty | Step-by-Step Gold Loan Interest Calculation Formula

Okay, deep breath! This is where we get practical. Most gold loans in India operate on a simple interest basis, which is great news because it’s much easier to calculate. Here’s the fundamental formula:

Simple Interest = (Principal Amount × Rate of Interest × Time) / 100

Let’s break down each component:

- Principal Amount (P): This is the initial amount of money you borrow against your gold.

- Rate of Interest (R): This is the annual interest rate quoted by your lender. It’s usually expressed as a percentage (e.g., 10% per annum). Important: Always convert this percentage to a decimal for calculation (e.g., 10% becomes 0.10, or 10/100).

- Time (T): This is the duration for which you borrow the money, expressed in years. If your loan is for 6 months, Time = 0.5 years. If it’s for 9 months, Time = 0.75 years.

Let’s Illustrate with an Example |

Suppose you take a gold loan of ₹1,00,000 at an annual interest rate of 12% for a tenure of 6 months.

P = ₹1,00,000

R = 12% per annum (or 0.12)

T = 6 months = 0.5 years

Simple Interest = (1,00,000 × 0.12 × 0.5)

Simple Interest = ₹6,000

So, for this 6-month loan, your total interest would be ₹6,000. Your total repayment would be Principal + Interest = ₹1,00,000 + ₹6,000 = ₹1,06,000.

Now, what about EMI calculation for gold loan? While many gold loans offer bullet repayment (pay principal and interest at the end), some do offer EMI options. If it’s an EMI, the interest component is typically calculated on the reducing principal balance. This means as you pay off parts of the principal with each EMI, the interest for the next period is calculated on a smaller outstanding amount. This is slightly more complex, but a good gold loan calculator can do this instantly for you.

Beyond the Numbers | Choosing the Right Gold Loan Repayment Options

Understanding the formula is great, but knowing how you can pay it back is just as crucial. Lenders often provide various gold loan repayment options, each with its own implications for your finances:

- Bullet Repayment: This is very common. You pay the entire principal amount and the accumulated interest at the end of the loan tenure. It’s excellent for those who expect a lump sum payment (like a bonus or maturity of an investment) to arrive before the loan ends.

- EMI (Equated Monthly Installment): Just like other loans, you pay a fixed amount every month, which includes both principal and interest. This is good for those with a steady income stream.

- Interest-Only Repayment: You pay only the interest monthly or periodically, and the principal amount at the end of the tenure. This keeps your monthly outgo low but requires a larger lump sum at the end.

- Partial Repayment: Some lenders allow you to pay back parts of the principal whenever you have extra funds, reducing your overall interest burden. This flexibility can be a massive advantage, especially if you’re looking at whether a gold loan is safe or risky for your specific needs.

Always discuss these options thoroughly with your lender and choose the one that aligns best with your financial capacity and expected cash flows. It’s part of the broader gold loan process that often gets overlooked.

Smart Moves | Tips for Getting the Best Gold Loan Rates

Now that you’re an interest calculation maestro, how do you ensure you’re getting a good deal? It’s not just about the formula; it’s about smart application.

- Compare, Compare, Compare: Don’t just walk into the first bank. Check rates from multiple banks and NBFCs. Their gold loan interest rates can vary significantly.

- Check Processing Fees: A low interest rate might be offset by high processing fees. Always look at the total cost of the loan.

- Understand Eligibility: While gold loan eligibility is generally simpler than, say, a personal loan, knowing the specific requirements of each lender can help you negotiate or choose better. Often, simply having a good credit score can subtly influence the rates offered, even for secured loans.

- Read the Fine Print: Seriously, I can’t stress this enough. Look for prepayment charges, late payment penalties, and any hidden clauses. This is where trustworthiness comes in; a transparent lender is always better.

- Leverage Online Calculators: Use an online gold loan calculator to quickly compare different scenarios (different amounts, tenures, and interest rates). This is an invaluable tool for financial planning.

Remember, a gold loan can be a powerful financial instrument when used wisely. It’s often a much more accessible and affordable option compared to something like ashort term personal loan online, especially if you have gold sitting idle. Knowing your numbers gives you confidence and control.

For more insights on financial planning and understanding various loan products, you can refer to reputable financial education portals likeInvestopedia, which often break down complex topics into easy-to-understand guides.

Your Burning Questions Answered | FAQ

What is the typical gold loan interest rate in India?

Gold loan interest rates in India typically range from 7% to 29% per annum, varying significantly between banks and NBFCs. Factors like the loan amount, tenure, LTV ratio, and lender’s policies all influence the final rate.

Can I pre-pay my gold loan?

Yes, most gold loans allow for prepayment. Many lenders, especially banks, do not charge prepayment penalties. However, it’s crucial to confirm this with your specific lender before taking the loan, as some NBFCs might have a lock-in period or charge a nominal fee.

How does a gold loan calculator help me?

A gold loan calculator is a fantastic tool that allows you to quickly estimate your interest payments and total repayment amount based on the principal, interest rate, and tenure. It helps you compare different loan offers and understand your financial commitment before applying.

What documents are needed for the gold loan process?

The gold loan process typically requires minimal documentation. You’ll generally need identity proof (e.g., Aadhar card, PAN card, Passport) and address proof (e.g., Aadhar card, electricity bill). Some lenders might also ask for income proof, though it’s less common for smaller gold loans.

Is a gold loan safe?

Yes, taking a gold loan from a regulated bank or NBFC is generally safe. Your gold is kept in secure vaults, and lenders follow strict guidelines set by the RBI. Always choose a reputable and licensed institution to ensure the safety of your valuable asset.

So, there you have it. The gold loan interest calculation formula isn’t some arcane secret reserved for financial wizards. It’s a simple, powerful tool that, once understood, puts you firmly in control of your borrowing decisions. Go forth, compare wisely, calculate confidently, and make your gold work smarter for you. Because knowing how your money works, my friend, is true financial freedom.