Let’s be honest, the thought of buying a home in the USA is exciting, isn’t it? The dream of your own space, a little slice of the American pie. But then, the reality hits: the mortgage application. And if you’re like many entrepreneurs, freelancers, or anyone whose income doesn’t come neatly packaged in a W-2, you’ve probably felt that pang of anxiety. How on earth do you get a home loan approval without income proof USA when every lender seems to demand pay stubs and tax returns that just don’t reflect your unique financial picture?

I get it. I’ve seen countless brilliant, successful individuals hit this wall, feeling sidelined by a system designed for a different era. The conventional wisdom says ‘no W-2, no mortgage.’ But here’s the thing: conventional wisdom isn’t always the full story. What if I told you there are legitimate, practical paths to homeownership for you, too? This isn’t about shady deals or loopholes; it’s about understanding the evolving landscape of mortgage lending and knowing where to look. Let’s dive in and demystify how you can achieve your homeownership dream, even without that traditional income documentation.

The Self-Employed Conundrum | Why Traditional Mortgages Don’t Always Fit

For most of us, when we think of a mortgage, we picture the standard, vanilla loan. You submit your employment history, your W-2s, your pay stubs, and tax returns for the last two years. The lender then calculates your debt-to-income (DTI) ratio, and if it all lines up, you’re golden. Simple, right? Well, not for everyone.

If you’re self-employed, an independent contractor, or a small business owner, your financial life is often more complex. You might have significant write-offs that dramatically reduce your taxable income, even if your gross revenue is fantastic. Or perhaps your income fluctuates, making a consistent monthly figure hard to pin down. This is where the system often fails those who contribute so much to the economy. Traditional lenders, bound by strict Qualified Mortgage (QM) rules, often struggle to see beyond the numbers on a tax return, leading to a frustrating dead-end for many aspiring homeowners seeking a no income verification mortgage .

This isn’t to say traditional lenders are bad; it’s just that their models aren’t built for your reality. They’re looking for predictability, and your dynamic income, while robust, might appear unpredictable on paper. But don’t despair! This is precisely why a new breed of lending products, specifically designed for people like you, has emerged. These aren’t just niche products; they’re becoming mainstream solutions for those who don’t fit the W-2 mold.

Your Secret Weapon | Understanding Non-QM and Alternative Lending

So, if traditional mortgages are out, what’s in? The answer often lies in what’s known asNon-QM loans(Non-Qualified Mortgages). These are mortgages that don’t meet the strict guidelines of a Qualified Mortgage, but they are absolutely legitimate and regulated. They simply offer more flexibility in how a lender assesses your ability to repay.

Within the Non-QM umbrella, you’ll find some incredibly powerful tools for securing a home loan approval without income proof USA . The most popular and widely available of these are:

- Bank Statement Loans: This is a game-changer for the self-employed. Instead of W-2s and tax returns, lenders will review 12 to 24 months of your personal or business bank statements. They’ll average your deposits over that period, often using a percentage (like 50% or 100% of deposits) as your qualifying income. It’s a direct, common-sense approach to proving your cash flow.

- Asset-Based Lending: If you’re a high-net-worth individual with significant liquid assets but less traditional income, this could be your path. Lenders look at your investment accounts, retirement funds, and other liquid assets to determine your ability to repay. They might “deplete” your assets over a certain number of years to calculate an imputed income.

- Investor Loans (DSCR Loans): For real estate investors, these are fantastic. The lender qualifies you based on the property’s potential rental income, not your personal income. If the property’s gross rental income covers its mortgage payment (Debt Service Coverage Ratio, or DSCR), you’re often approved. This is a common route for those building a portfolio and often requires minimal personal income documentation.

These non-QM loans represent a vital shift in the lending industry, acknowledging the diverse ways people earn and manage their money. When you’re exploring these options, it’s also a good idea to understand your potential monthly payments. You can easily estimate what your mortgage might look like with anEMI calculator, helping you budget and plan for your future home, regardless of your income verification method.

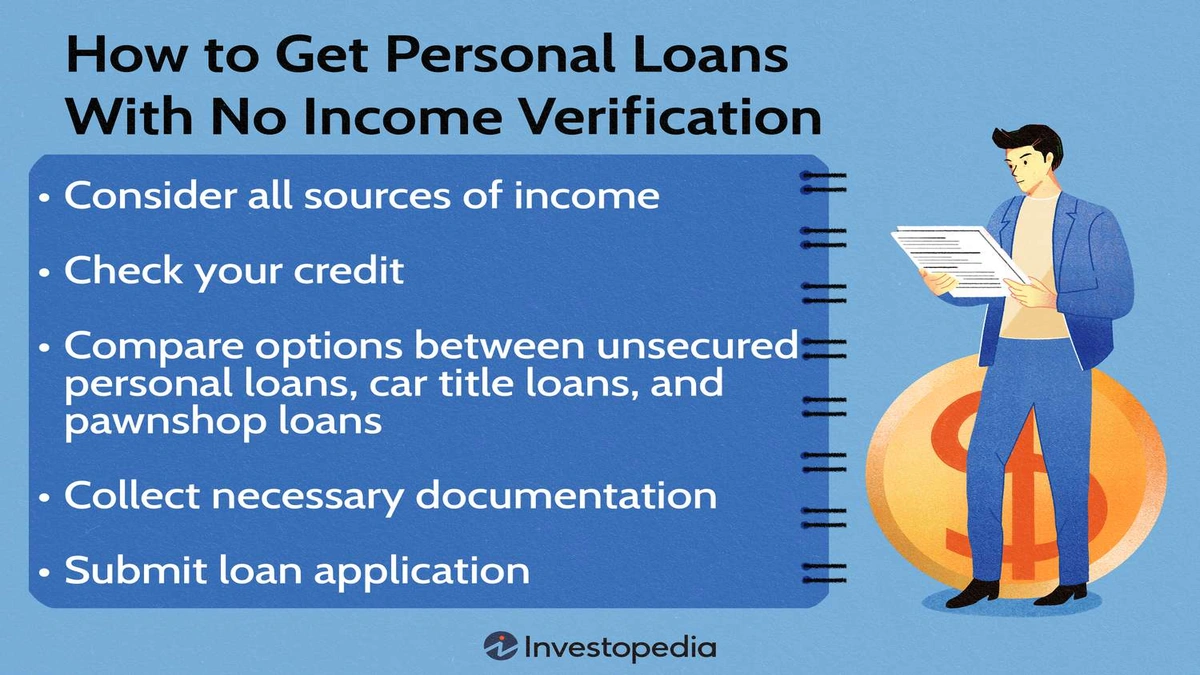

Beyond the Paystub: Practical Paths to Home Loan Approval Without Income Proof USA

Let’s get practical. How do these alternative options actually work, and what do you need to prepare? This is where your strategy comes into play, especially for self-employed home loans .

The Power of Bank Statement Loans

As mentioned, bank statement loans are the most common solution for self-employed individuals. Lenders typically ask for:

- 12 to 24 months of bank statements: Both personal and business, depending on how your income flows. Consistency is key here.

- Proof of self-employment: Business license, articles of incorporation, or a letter from your CPA.

- Good credit score: Generally, you’ll need a FICO score of 620-680 or higher, depending on the lender and loan terms.

- Down payment: While not always higher than traditional loans, expect to put down at least 10-20%.

The beauty of this is that it looks at your actual cash flow, not just your taxable income after deductions. It’s a much more realistic picture for many entrepreneurs. This is truly one of the best alternative mortgage options out there.

Asset Depletion and Asset-Based Lending

For those with substantial wealth but perhaps fluctuating income, asset-based lending can be a lifesaver. Lenders will look at your portfolio of liquid assets – stocks, bonds, mutual funds, retirement accounts (like 401ks or IRAs) – and calculate an income based on a percentage of those assets over a set period (e.g., 20-30 years). This is often ideal for retirees with large nest eggs but no active employment income, or for high-net-worth individuals managing investments.

Debt Service Coverage Ratio (DSCR) Loans for Investors

If your goal is to buy an investment property, then a DSCR loan is your go-to. This particular type of investor loan doesn’t care about your personal income or DTI. It focuses solely on the property’s ability to generate enough rental income to cover its own expenses, including the mortgage. If the property can “pay for itself,” you’re in a strong position. It’s an excellent solution for expanding your real estate portfolio without impacting your personal income statements.

While the old stated income loans (where you simply stated your income without verification) are largely a thing of the past due to regulatory changes post-2008, these modern alternative financing solutions are fully compliant and designed to serve a real market need.

Navigating the Landscape | Tips for Success

Okay, so you know the options are there. Now, how do you actually make it happen? Here are some insider tips:

- Find a Specialized Lender: This is crucial. Don’t waste your time with a lender who only offers conventional loans. Seek out mortgage brokers or banks that specifically advertise Non-QM loans, bank statement loans, or mortgage for self-employed products. They understand the nuances and can guide you.

- Prepare Your Finances Meticulously: For bank statement loans, ensure your statements are clean and consistent. Avoid large, unexplained deposits or frequent overdrafts. For asset-based loans, have clear statements of your liquid assets.

- Build a Strong Credit Score: Even with alternative income verification, a good credit score (typically 680+) will always get you better rates and terms. This shows overall financial responsibility.

- Be Ready for a Down Payment: While some programs offer lower down payments, having 10-20% (or more) significantly strengthens your application and can lead to better interest rates.

- Keep Your Debt Low: Even if DTI is calculated differently, having less existing debt always makes you a more attractive borrower.

- Consider a Co-Borrower: If you have a spouse or partner with more traditional income, adding them to the loan application can open up more options.

Just as businesses often explore variousbusiness expansion loan options, individuals need to be savvy about their personal financing. The key is to be informed and proactive. The market is dynamic, and with the right approach, your dream of homeownership in the USA is absolutely within reach.

FAQ | Your Burning Questions Answered

Are “stated income loans” still a thing for home loan approval without income proof USA?

Not in their original form. The “stated income, stated asset” loans that were prevalent before the 2008 financial crisis largely disappeared due to new regulations. Today’s non-QM loans, like bank statement loans, are legitimate and require thorough documentation of assets or cash flow, just not traditional W-2s or tax returns.

What’s the biggest hurdle for self-employed mortgage applicants?

The primary hurdle is often the lender’s inability to accurately assess income from tax returns that show significant write-offs. This is precisely where bank statement loans and asset-based lending come in, offering a more realistic view of the applicant’s financial health.

How much of a down payment do I need for a no income verification mortgage?

While it varies by lender and loan product, expect to put down anywhere from 10% to 20% or even more. Generally, a larger down payment can offset the perceived risk of alternative income verification, potentially leading to better terms.

Can I use a bank statement loan for my primary residence?

Absolutely! Bank statement loans are primarily designed for owner-occupied primary residences, though some lenders also offer them for second homes and investment properties. They are a fantastic option for self-employed individuals looking to buy their main home.

Are interest rates higher for these alternative financing solutions?

Generally, yes, interest rates for non-QM loans and other alternative solutions can be slightly higher than for conventional, fully documented mortgages. This is because they carry a slightly higher perceived risk for the lender. However, the difference is often manageable and worth it for the flexibility they provide.

So, there you have it. The path to home loan approval without income proof USA isn’t a myth; it’s a reality paved with specific, legitimate lending products designed for the modern economy. It requires a bit more research and finding the right specialized lender, but the dream of owning a home in the United States, whether you’re a bustling entrepreneur, a savvy investor, or a financially stable individual whose income simply doesn’t fit the traditional box, is absolutely achievable. Don’t let old-school thinking hold you back. Your home is waiting.