So, you’re eyeing that perfect pre-owned car, right? Maybe it’s a reliable sedan for daily commutes or a spacious SUV for family adventures. Whatever it is, the dream often hits a speed bump when we start thinking about financing. Specifically, those pesky used car loan interest rates USA . Let’s be honest, it can feel like a labyrinth, with different lenders, varying terms, and a whole lot of jargon thrown your way. But what if I told you it doesn’t have to be? What if you could walk into a dealership or apply online feeling genuinely confident, armed with the knowledge to get the best deal?

That’s exactly what we’re going to do today. Forget the dry financial reports; consider me your guide, helping you cut through the noise and understand exactly how to secure favorable auto loan rates for your next used car. We’re not just talking about what the rates are , but how you can influence them, what to look out for, and why some deals are better than others. Because, let’s face it, a few percentage points here or there can mean hundreds, even thousands, of dollars over the life of your loan. And who wouldn’t want to keep that cash in their pocket?

Decoding Average Used Car Loan Interest Rates | What’s the Benchmark?

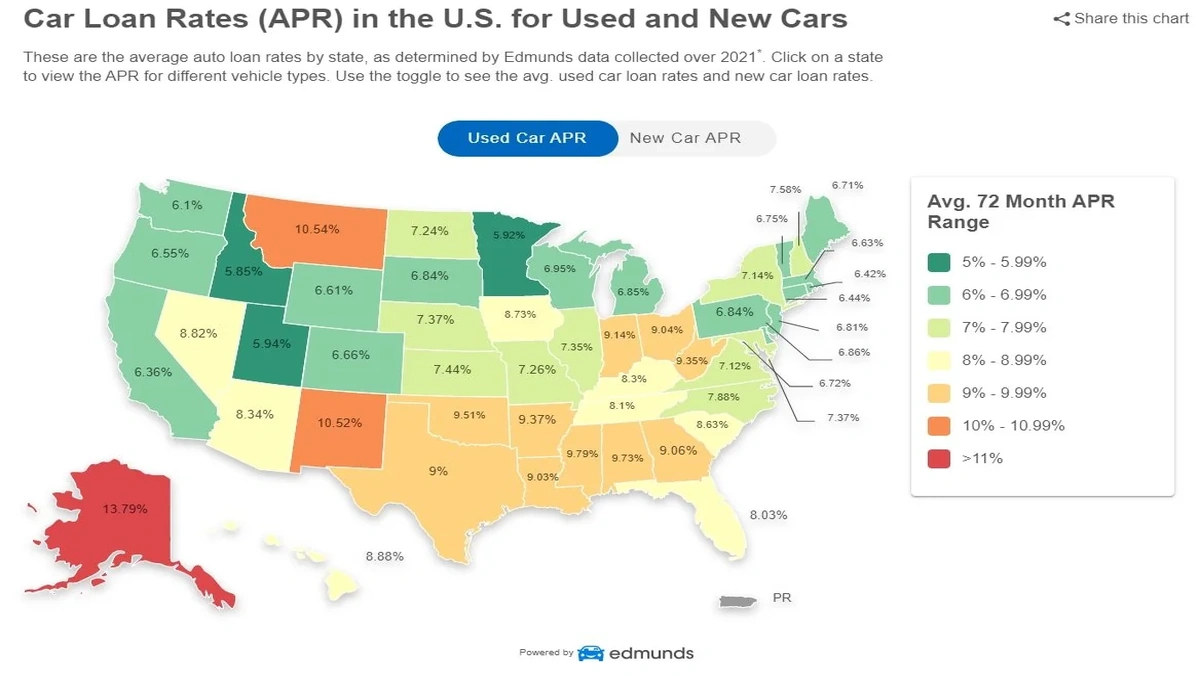

First things first, let’s talk numbers. What’s the typical playing field for used car loan interest rates in the USA? Well, it’s not a single, fixed number. It’s a spectrum, heavily influenced by a few key factors we’ll dive into. Generally speaking, for a well-qualified borrower (think excellent credit), used car loan interest rates can range from the low single digits (say, 4-6%) up to double digits (10-15% or even higher) for those with less-than-stellar credit or for older vehicles. The average often hovers somewhere in the 7-9% range for a decent credit score, but this is a moving target, much likehigher education loanrates.

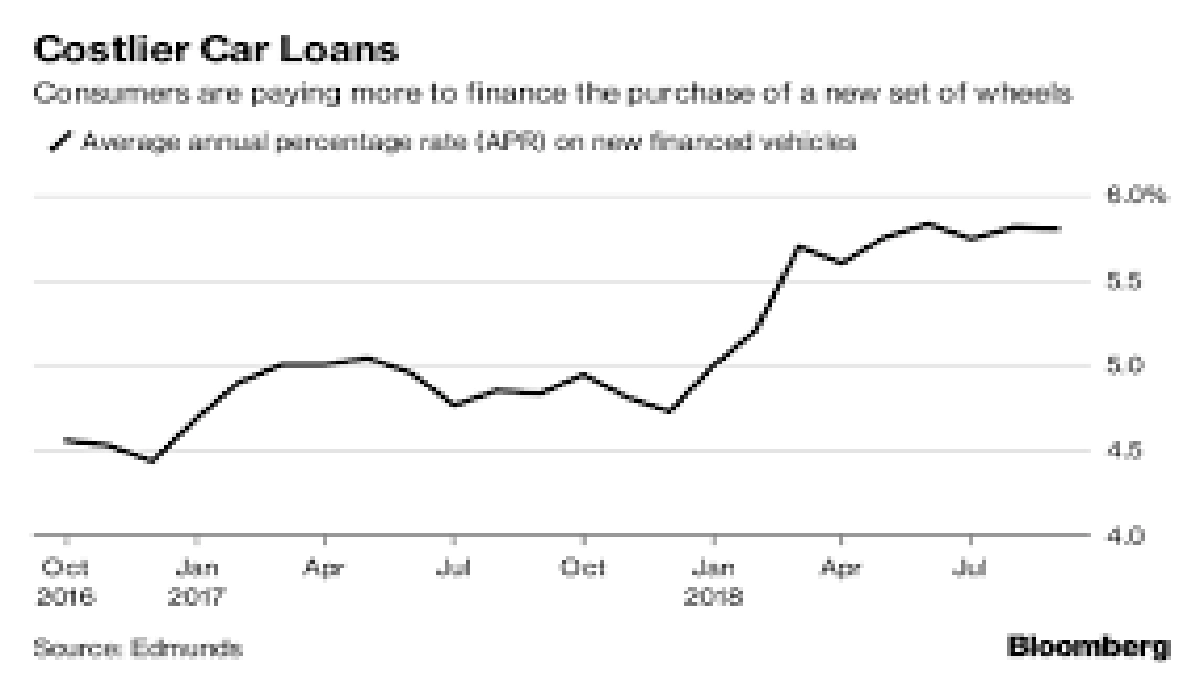

What fascinates me about these numbers is how much they fluctuate. Economic conditions, the Federal Reserve’s policies, and even the competitive landscape among car loan lenders all play a role. For instance, if the Fed raises its benchmark rates, you can almost guarantee that consumer loan rates, including those for financing a used car , will eventually follow suit. So, staying informed isn’t just a good idea; it’s a strategic move.

But here’s the thing: knowing the average is just the starting point. Your personal rate will depend on your unique financial profile and the specifics of the car you’re buying. This is where the real strategy comes in.

Your Credit Score | The Unsung Hero of Low Interest Rates

If there’s one single factor that will have the most profound impact on your used car loan interest rates USA , it’s your credit score . Period. Lenders use your credit score as a quick snapshot of your financial reliability. A higher score (generally 700+) signals less risk, meaning lenders are more willing to offer you lower rates. Conversely, a lower score (below 600) suggests higher risk, leading to higher rates to compensate the lender.

I’ve seen countless people overlook this, thinking their credit score is set in stone. But it’s not! Before you even start seriously shopping for a car, pull your credit report from all three major bureaus (Experian, TransUnion, Equifax). You can get a free report annually. Check for errors, pay down any outstanding debts, and avoid opening new lines of credit. Even a 50-point bump in your score can translate into significant savings on your interest rate . It’s like preparing for an exam; you wouldn’t just show up without studying, would you? Preparing your credit is your study guide forgetting the best loan terms.

For those with bad credit used car loans , don’t despair. While your rates might be higher initially, there are still options. You might need to accept a higher rate for a shorter loan term , make a larger down payment , or consider a co-signer. The goal is to get approved, make timely payments, and then potentially refinance your used car loan down the line when your credit score improves. It’s a marathon, not a sprint.

Beyond Credit | Other Factors Affecting Your Car Loan Rates

While your credit score is king, it’s not the only player on the field. Several other elements influence the used car loan interest rates you’ll be offered:

- Loan Term: This is the length of time you have to repay the loan. Shorter terms (e.g., 36 months) typically have lower interest rates but higher monthly payments. Longer terms (e.g., 60-72 months) often come with higher rates but lower monthly payments. My advice? Balance the lowest possible rate with a monthly payment you can comfortably afford. Don’t stretch the term just to lower the payment if it means paying significantly more in interest overall.

- Down Payment: The more money you put down upfront, the less you need to borrow. This reduces the lender’s risk and can lead to a lower interest rate. A solid down payment used car is often 10-20% of the car’s value.

- Vehicle Age and Mileage: Lenders view older cars with high mileage as riskier because they might break down more often, potentially leaving you with a loan on a non-functional asset. This can mean higher rates.

- Debt-to-Income Ratio (DTI): This ratio compares your monthly debt payments to your gross monthly income. Lenders want to see a manageable DTI, ideally below 36%, to ensure you can handle the new car payment.

- Market Conditions: As mentioned, the broader economic environment and the Federal Reserve’s actions directly impact interest rates across the board.

Understanding these variables helps you negotiate better and choose the right used car financing options . It’s not just about what the bank offers; it’s about what you bring to the table.

The ‘How-To’ of Securing the Best Rates

Okay, so we’ve talked about the ‘why’ and the ‘what.’ Now, let’s get to the ‘how.’ This is your actionable game plan for getting the best possible used car loan interest rates USA :

- Get Pre-Approved: This is arguably the most crucial step. Before you even set foot in a dealership, apply for pre-approval from banks, credit unions, and online lenders. Why? Because it gives you a benchmark. You’ll know what kind of rate you qualify for, turning you into a cash buyer at the dealership. This takes the focus off the monthly payment and puts it squarely on the car’s price, empowering you to negotiate better. Many reputable institutions offer an online car loan application process that is quick and easy.

- Shop Around Aggressively: Don’t just take the first offer, especially not from the dealership’s finance department. While they can sometimes match or beat outside offers, their initial offer might not be the best. Compare at least 3-4 different offers. This competition forces lenders to give you their most competitive APR. Remember, they want your business!

- Boost Your Credit Score (If Possible): As discussed, even a small improvement can make a difference. Pay bills on time, reduce credit card balances, and avoid new credit inquiries in the months leading up to your car purchase.

- Make a Larger Down Payment: If you can afford it, putting down more cash upfront reduces your loan amount and signals financial stability to lenders, often resulting in a lower interest rate.

- Consider a Shorter Loan Term: While it means higher monthly payments, a shorter loan term almost always comes with a lower interest rate and less total interest paid over time. Use a car loan calculator to see how different terms affect your total cost.

- Know the Car’s Value: Research the market value of the used car you’re interested in using sites like Kelley Blue Book or Edmunds. This ensures you’re not overpaying, which can negatively impact your loan-to-value ratio and, consequently, your rate.

This process might seem like a lot of work, but trust me, the savings are worth it. Just like understanding how agold loan works step by step, knowing the ins and outs of auto financing empowers you.

Frequently Asked Questions About Used Car Loans

Your Burning Questions Answered

What is a good credit score for a used car loan?

Generally, a credit score of 660 or higher is considered good, while 700+ is excellent and will likely qualify you for the best used car loan interest rates USA . However, you can still get a loan with lower scores, though the interest rate will be higher.

Are used car loan rates higher than new car loan rates?

Yes, typically, used car loan interest rates are slightly higher than new car loan rates. This is because used cars are considered a higher risk by lenders due to their age, mileage, and potential for mechanical issues.

How can I lower my interest rate on a used car loan?

You can lower your rate by improving your credit score, making a larger down payment, choosing a shorter loan term, shopping around for multiple offers, and potentially refinancing your loan later on.

Should I get pre-approved for a used car loan?

Absolutely! Getting pre-approved is highly recommended. It gives you a clear understanding of what you can afford, provides leverage for negotiation at the dealership, and often streamlines the buying process.

What is APR and how does it relate to interest rates?

APR stands for Annual Percentage Rate. It’s a broader measure of the cost of borrowing money, including not just the interest rate but also other fees and charges associated with the loan. When comparing loan offers, always look at the APR for a more accurate comparison of the total cost.

So, there you have it. The world of used car loan interest rates USA isn’t nearly as intimidating when you know the ropes. By taking the time to understand your credit, shop around, and prepare your finances, you’re not just getting a car; you’re making a smart financial decision. Go forth, get that dream car, and drive away knowing you secured the best possible deal. Happy driving!